Municipalities

Urban Local Government (ULG) in India has evolved significantly over time, culminating in a structured system established by the 74th Constitutional Amendment Act in 1992. Here’s an overview of key aspects related to urban local governments, their evolution, and historical context:

Types of Urban Local Governments

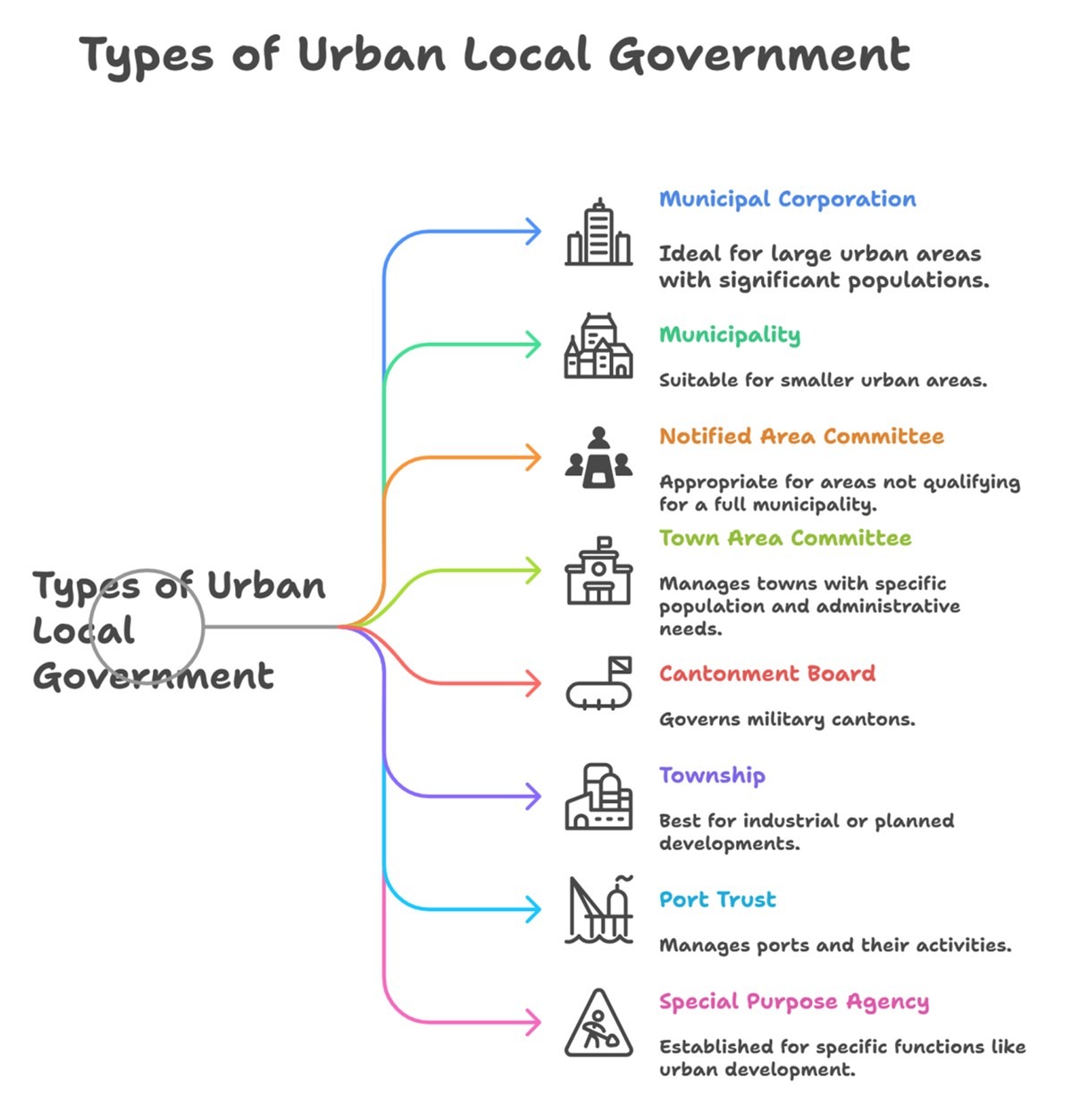

In India, there are eight recognized types of urban local governments:

- Municipal Corporation: Governs large urban areas with more significant populations.

2. Municipality: Governs smaller urban areas.

3. Notified Area Committee: Created for areas that may not qualify for a full municipality.

4. Town Area Committee: Manages towns with a specific population and administrative requirements.

5. Cantonment Board: Governs military cantons.

6. Township: Industrial or planned developments with administrative powers.

7. Port Trust: Manages ports and their activities.

8. Special Purpose Agency: Established for specific areas or functions, such as urban development or infrastructure improvement.

Committees and Commissions

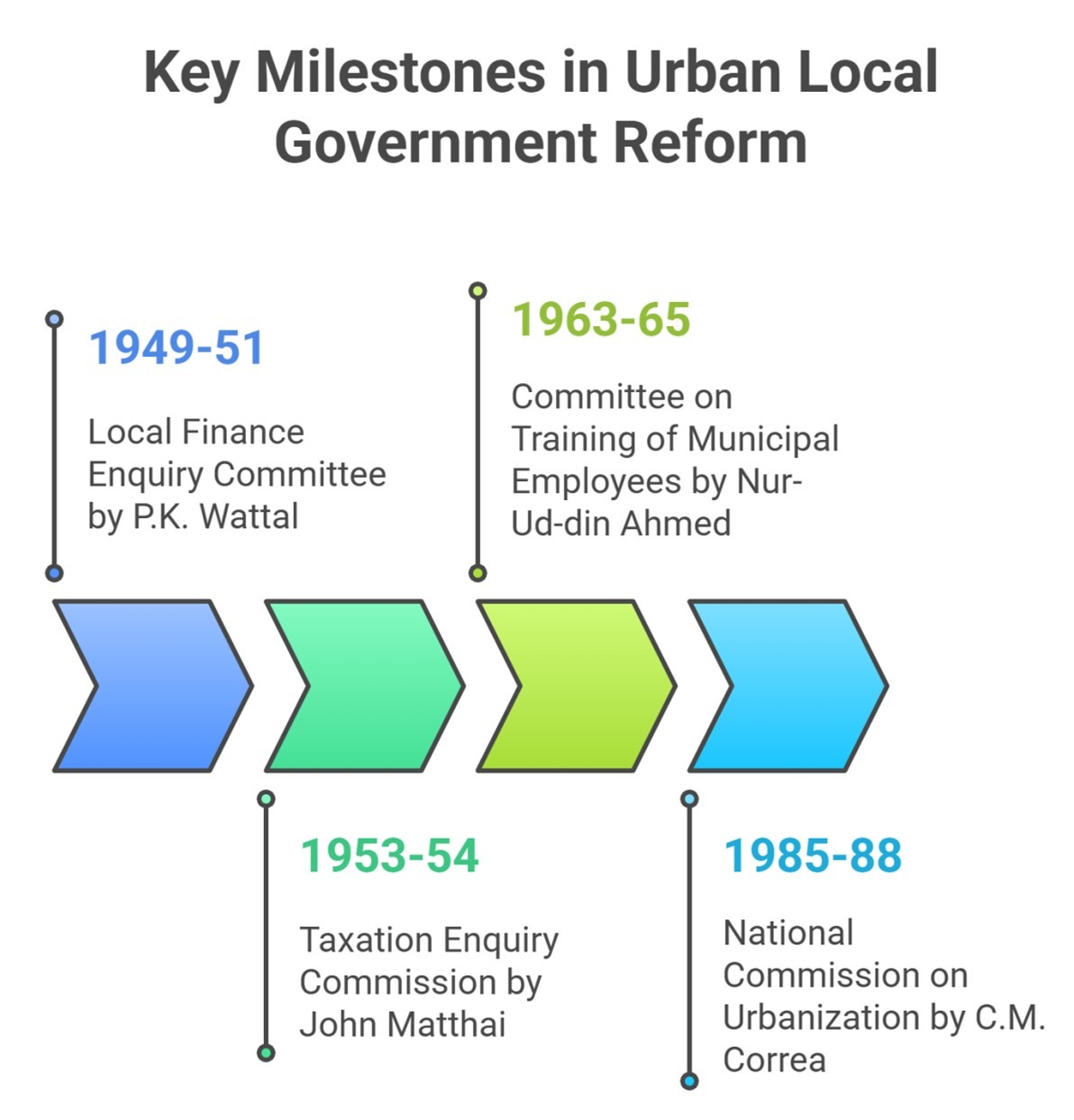

Numerous committees and commissions have been appointed over the years to assess and improve urban local government functioning. Some notable ones include:

- Local Finance Enquiry Committee (1949-51)– P.K. Wattal

- Taxation Enquiry Commission (1953-54)– John Matthai

- Committee on the Training of Municipal Employees (1963-65)– Nur-Ud-din Ahmed

- National Commission on Urbanization (1985-88)– C.M. Correa

Constitutionalisation

The push for constitutional recognition began with the 65th Constitutional Amendment Bill (Nagarpalika Bill) introduced in 1989, which sought to grant municipal bodies constitutional status. Although it passed in the Lok Sabha, it was ultimately defeated in the Rajya Sabha.

- In September 1990, a revised version of the Nagarpalika Bill was proposed but lapsed due to the dissolution of the Lok Sabha.

- The P.V. Narasimha Rao Government introduced a modified Municipalities Bill in September 1991, which ultimately led to the passage of the 74th Constitutional Amendment Act in 1992, enacted in 1993.

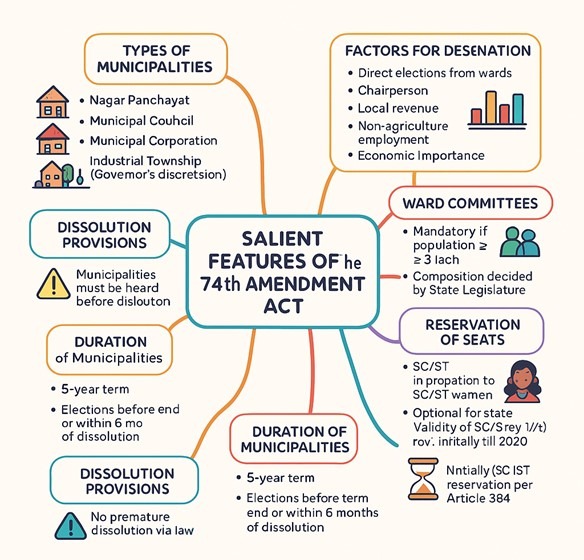

Salient Features of the 74th Amendment Act

1. Types of Municipalities:

- The Act prescribes three types of municipalities:

- Nagar Panchayat: For transitional areas.

- Municipal Council: For smaller urban areas.

- Municipal Corporation: For larger urban areas.

- There is a provision for the governor to designate certain areas as industrial townships if municipal services are provided by an industrial establishment, thereby exempting them from the municipality classification.

- The Act prescribes three types of municipalities:

2. Factors for Designation:

- The governor must consider several factors while designating a transitional area, smaller urban area, or larger urban area:

- Density of population.

- Revenue generated for local administration.

- Employment percentage in non-agricultural sectors.

- Economic importance.

- Any other relevant factors.

- The governor must consider several factors while designating a transitional area, smaller urban area, or larger urban area:

3. Composition and Elections:

- Members of the municipality are directly elected by the people from designated wards.

- State legislatures can dictate the manner of electing the chairperson and provide for representation of:

- Experts in municipal administration without voting rights.

- Members of the Lok Sabha and state legislative assemblies representing the municipal area.

- Members of the Rajya Sabha and state legislative councils registered as voters in the area.

- Chairpersons of committees (excluding ward committees).

4. Wards Committees:

- For municipalities with a population of three lakh or more, ward committees must be established.

- The state legislature can define the composition and operational framework of these committees.

5. Other Committees:

- States can form additional committees, with chairpersons being eligible for membership in the municipality.

6. Reservation of Seats:

- The Act mandates the reservation of seats for Scheduled Castes (SCs) and Scheduled Tribes (STs) in proportion to their population in the municipality.

- A minimum of one-third of total seats must be reserved for women, including women from SCs and STs.

- States can also reserve seats for backward classes.

- Reservations for SC/ST seats will expire after the period defined in Article 334, which is currently set until 2020 (this may need further amendments as this period has passed).

7. Duration of Municipalities:

- Each municipality has a five-year term. However, it can be dissolved earlier.

- Elections must be conducted before the term expires or within six months of dissolution, unless the remaining term is less than six months.

- Newly constituted municipalities following dissolution serve the remaining duration of the previous body.

8. Dissolution Provisions:

- Municipalities must be given a reasonable opportunity to represent their case before being dissolved.

- No amendment of existing laws can lead to the dissolution of a municipality before the end of its five-year term.

Types of Urban Governments

1. Municipal Corporation:

- Established for large cities such as Delhi, Mumbai, Kolkata, and Bangalore.

- Governed by state acts or acts of Parliament in the case of union territories.

- Comprises three authorities:

- Council: The legislative body consisting of elected councillors and nominated experts, led by a Mayor.

- Standing Committees: Focus on specific issues such as health and finance.

- Municipal Commissioner: The chief executive, responsible for implementing council decisions, usually an IAS officer.

2. Municipality:

- Created for smaller towns and cities, known by various names (e.g., municipal council).

- Similar structure to municipal corporations, with a council, standing committees, and a chief executive officer.

- The council is headed by a president or chairperson who has significant executive powers.

3. Notified Area Committee:

- Formed for rapidly developing areas or towns that do not meet full municipal criteria but are deemed important.

- Established via a notification in the government gazette and operates under the State Municipal Act.

- Composed entirely of nominated members appointed by the state government.

4. Town Area Committee:

- Established for small towns with limited civic functions such as drainage and street lighting.

- Its governance and composition are defined by specific state legislation and can be wholly elected, wholly nominated, or a mix of both.

5. Cantonment Board:

- Administers civilian areas in cantonments under the Cantonments Act of 2006, managed by the Central government.

- Consists of elected and nominated members, with a military officer serving as the ex-officio president.

- Functions similarly to municipalities with obligatory and discretionary responsibilities.

6. Township:

- Established by large public enterprises to provide civic amenities for employees living in housing colonies.

- Operates under a town administrator appointed by the enterprise with no elected members, being an extension of the organization’s bureaucratic structure.

7. Port Trust:

- Created to manage ports and provide civic amenities in port areas such as Mumbai and Chennai.

- Governed by an act of Parliament, includes both elected and nominated members, with an official serving as the chairman.

8. Special Purpose Agency:

- These are functional bodies created to address specific urban needs that fall under municipal responsibilities, such as urban development authorities and housing boards.

- They operate independently of traditional municipal governments and are established by acts of state legislatures or executive resolutions.

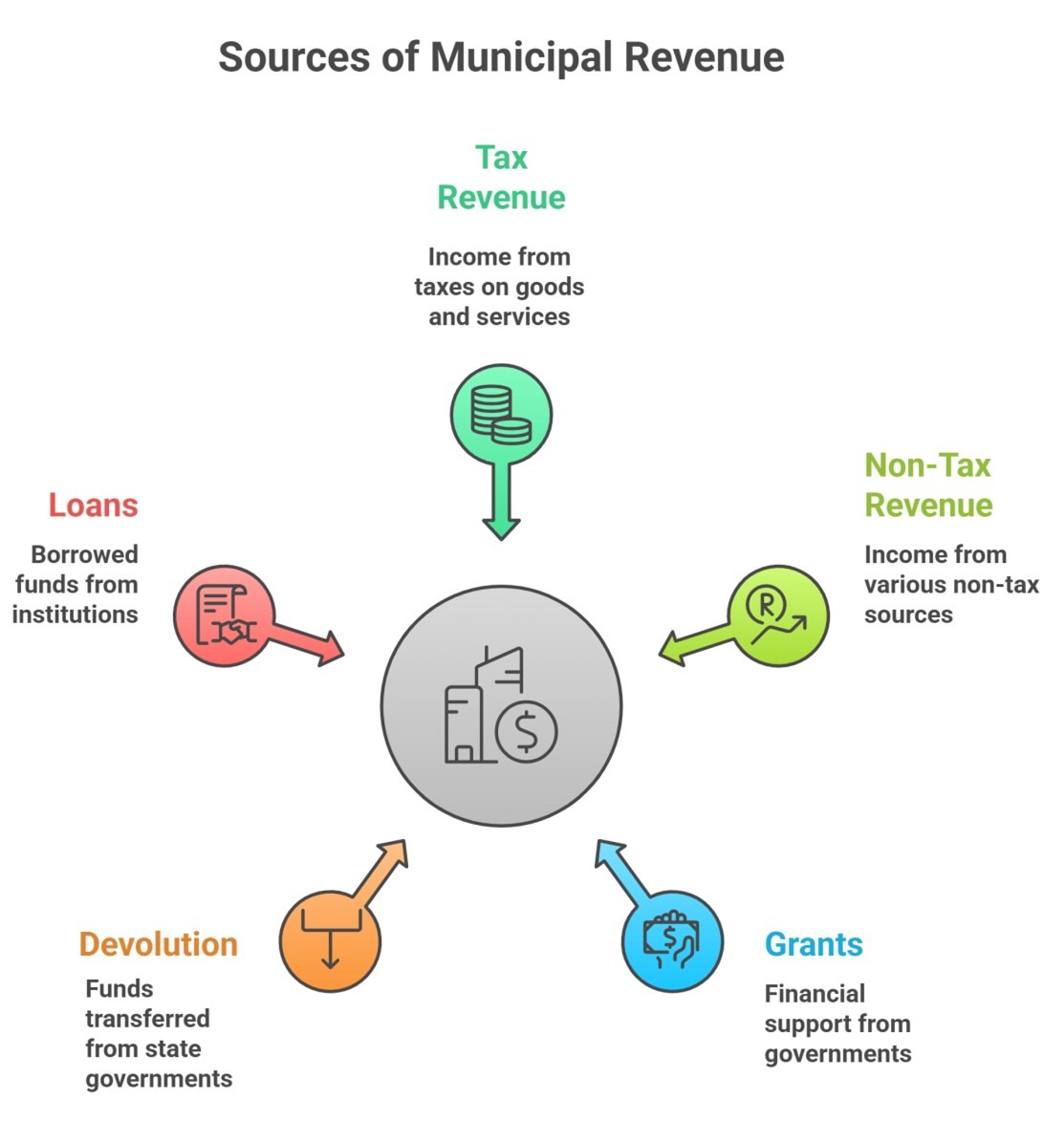

Sources of Municipal Revenue

1. Tax Revenue:

- Urban local bodies generate income through various local taxes, including:

- Property Tax: The most significant source of revenue.

- Entertainment Tax: Collected on entertainment events and activities.

- Taxes on Advertisements: Charged for advertisements placed in public areas.

- Professional Tax: Levied on professionals and businesses.

- Water Tax, Lighting Tax: Charges for public utilities.

- Octroi: Tax on goods entering a local area (mostly abolished in many states).

- Other specific cesses may include library cess, education cess, and beggary cess.

- Urban local bodies generate income through various local taxes, including:

2. Non-Tax Revenue:

- This includes various income sources such as:

- Rent on Municipal Properties: Income from properties owned by the municipality.

- Fees and Fines: Charges imposed for services and penalties for violations.

- User Charges: Fees collected for utilities like water supply and sanitation.

- Royalties and Profits: Earnings from municipal enterprises.

- This includes various income sources such as:

3. Grants:

- Financial support from the Central and State Governments for development programs, infrastructure, and urban reform initiatives.

4. Devolution:

- Funds transferred to urban local bodies from state governments based on recommendations made by the State Finance Commission.

5. Loans:

- Urban local bodies may borrow from state governments and financial institutions, typically requiring state approval.

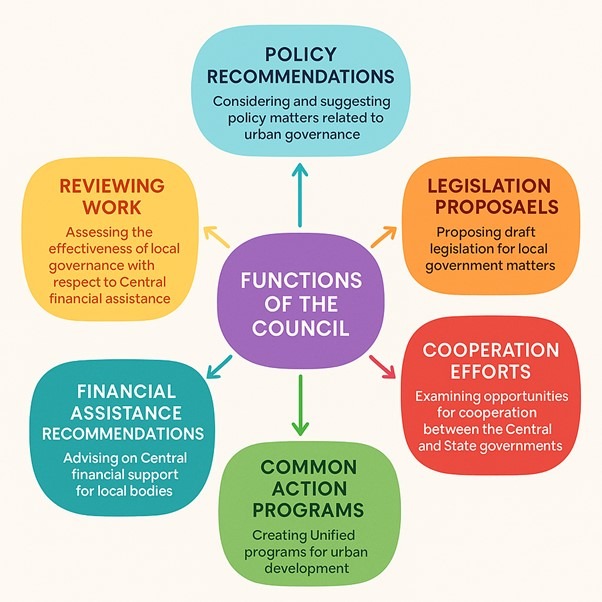

Central Council of Local Government

The Central Council of Local Government was established in 1954 under Article 263 of the Constitution of India. Initially named the Central Council of Local Self-Government, it focuses solely on urban local governance following its reconfiguration in the 1980s.

Functions of the Council:

- Policy Recommendations: Considering and suggesting policy matters related to urban governance.

- Legislation Proposals: Proposing draft legislation for local government matters.

- Cooperation Efforts: Examining opportunities for cooperation between the Central and State governments.

- Common Action Programs: Creating unified programs for urban development.

- Financial Assistance Recommendations: Advising on Central financial support for local bodies.

- Reviewing Work: Assessing the effectiveness of local governance with respect to Central financial assistance.