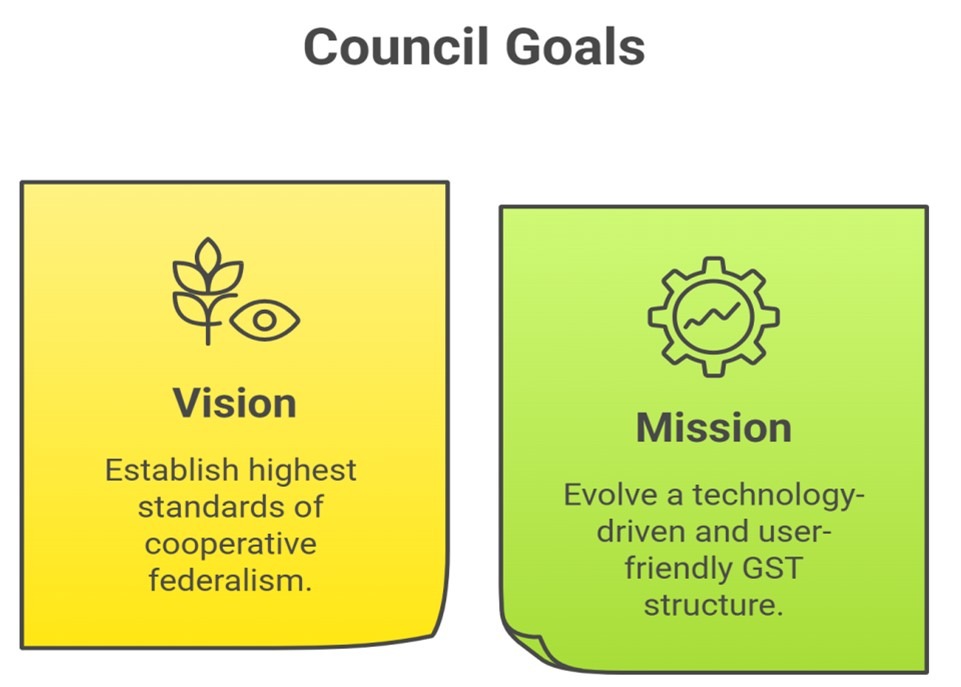

Vision and Mission of the Council

The Council is tasked with guiding the implementation of GST and ensuring a harmonized tax structure across the country. The vision and mission reflect its commitment to cooperative governance:

- Vision: To establish the highest standards of cooperative federalism in the functioning of the Council as the first constitutional federal body empowered to make significant decisions regarding GST.

- Mission: To evolve a GST structure that is technology-driven, user-friendly, and developed through a process of extensive consultation with stakeholders.

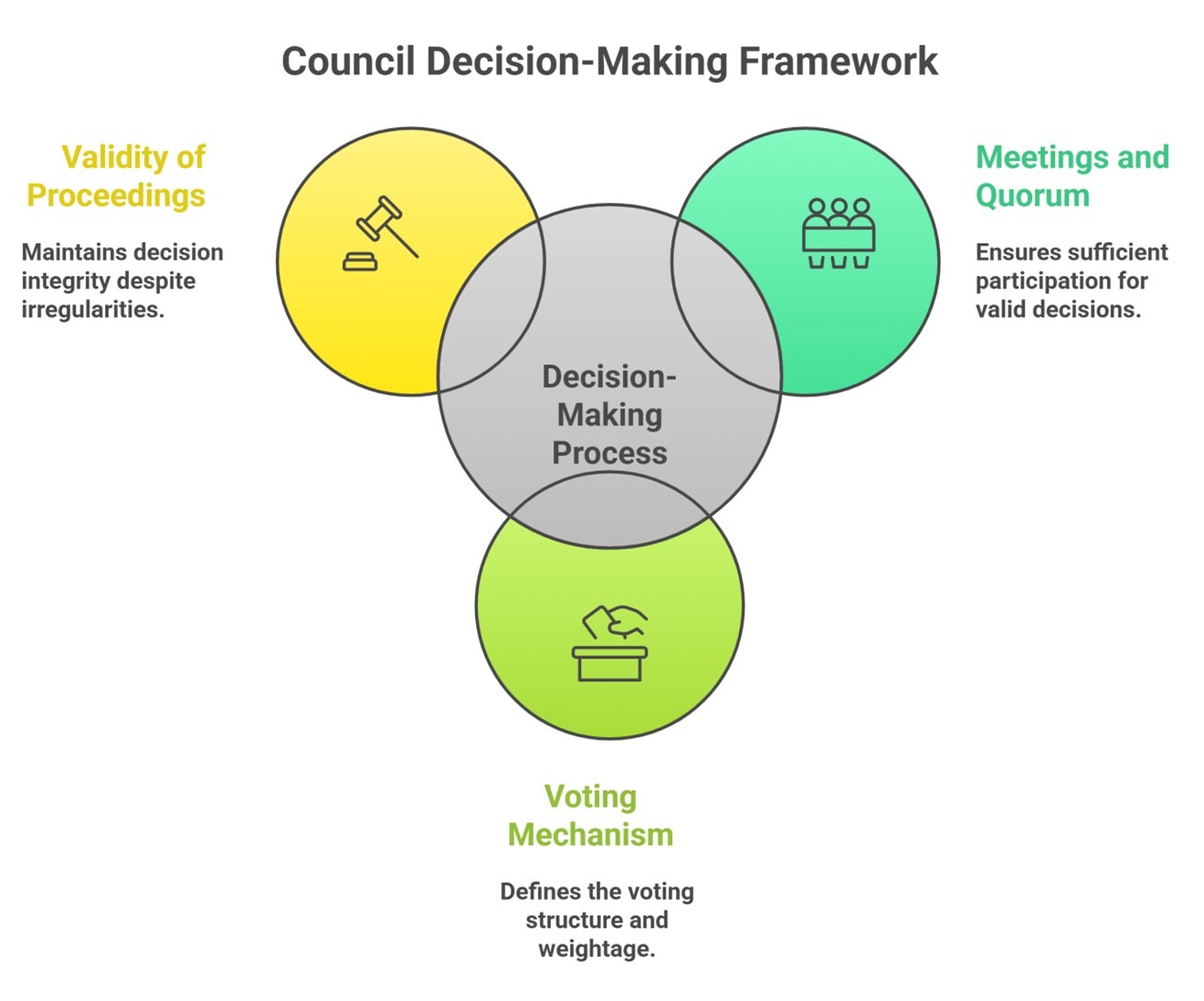

Decision-Making Process

Meetings and Quorum:

- Decisions of the Council are made during its meetings. A quorum for a meeting requires one-half of the total number of Council members to be present.

Voting Mechanism:

- Decisions are taken based on a majority of not less than three-fourths of the weighted votes of the members present and voting. The voting weightage is distributed as follows:

- The Central Government’s vote holds a weightage of one-third of the total votes cast.

- The combined votes of all State Governments hold a weightage of two-thirds of the total votes cast.

- Decisions are taken based on a majority of not less than three-fourths of the weighted votes of the members present and voting. The voting weightage is distributed as follows:

Validity of Proceedings:

- The actions or proceedings of the Council remain valid even if:

- There is any vacancy or defect in its constitution.

- There are defects in the appointment of members.

- There are procedural irregularities that do not affect the merits of the decision.

- The actions or proceedings of the Council remain valid even if:

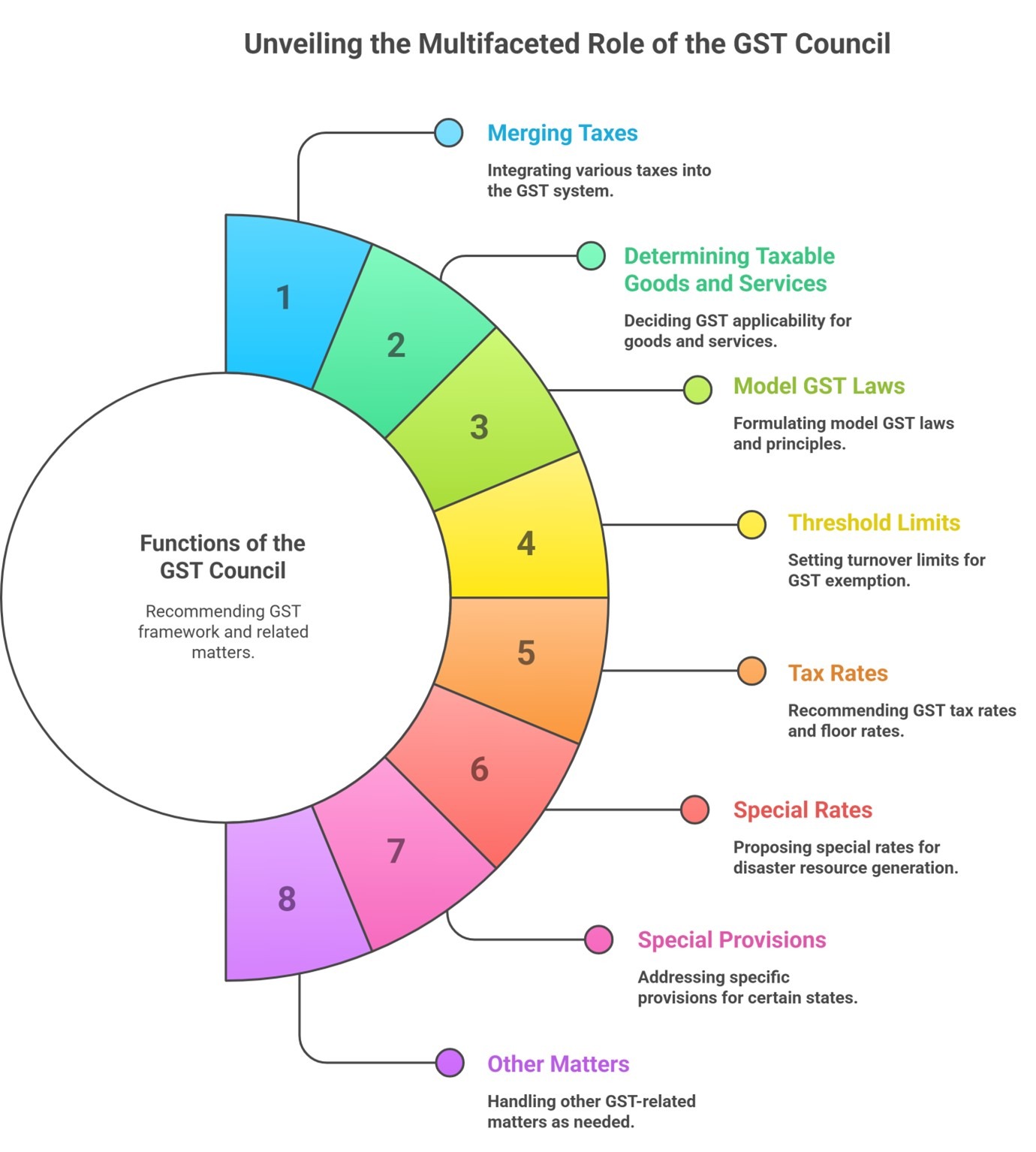

Functions of the GST Council

The GST Council is tasked with making various recommendations concerning the GST framework. These recommendations include:

1. Merging Taxes:

- Identifying the taxes, cesses, and surcharges imposed by the Centre, states, and local bodies that will be integrated into the GST.

2. Determining Taxable Goods and Services:

- Deciding which goods and services may be either subjected to GST or exempted from it.

3. Model GST Laws:

- Formulating model GST laws, along with principles regarding levy, apportionment of GST on interstate trade and commerce, and the principles governing the place of supply.

4. Threshold Limits:

- Setting the threshold limit of turnover below which certain goods and services may be exempted from GST.

5. Tax Rates:

- Recommending the tax rates, including setting floor rateswith bands of GST.

6. Special Rates:

- Proposing special rates that may be levied for a specified period to generate additional resources during natural disasters or calamities.

7. Special Provisions:

- Making provisions specifically addressing states like Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh, and Uttarakhand.

8. Other Matters:

- Addressing any other matters related to GST, as deemed necessary by the Council.

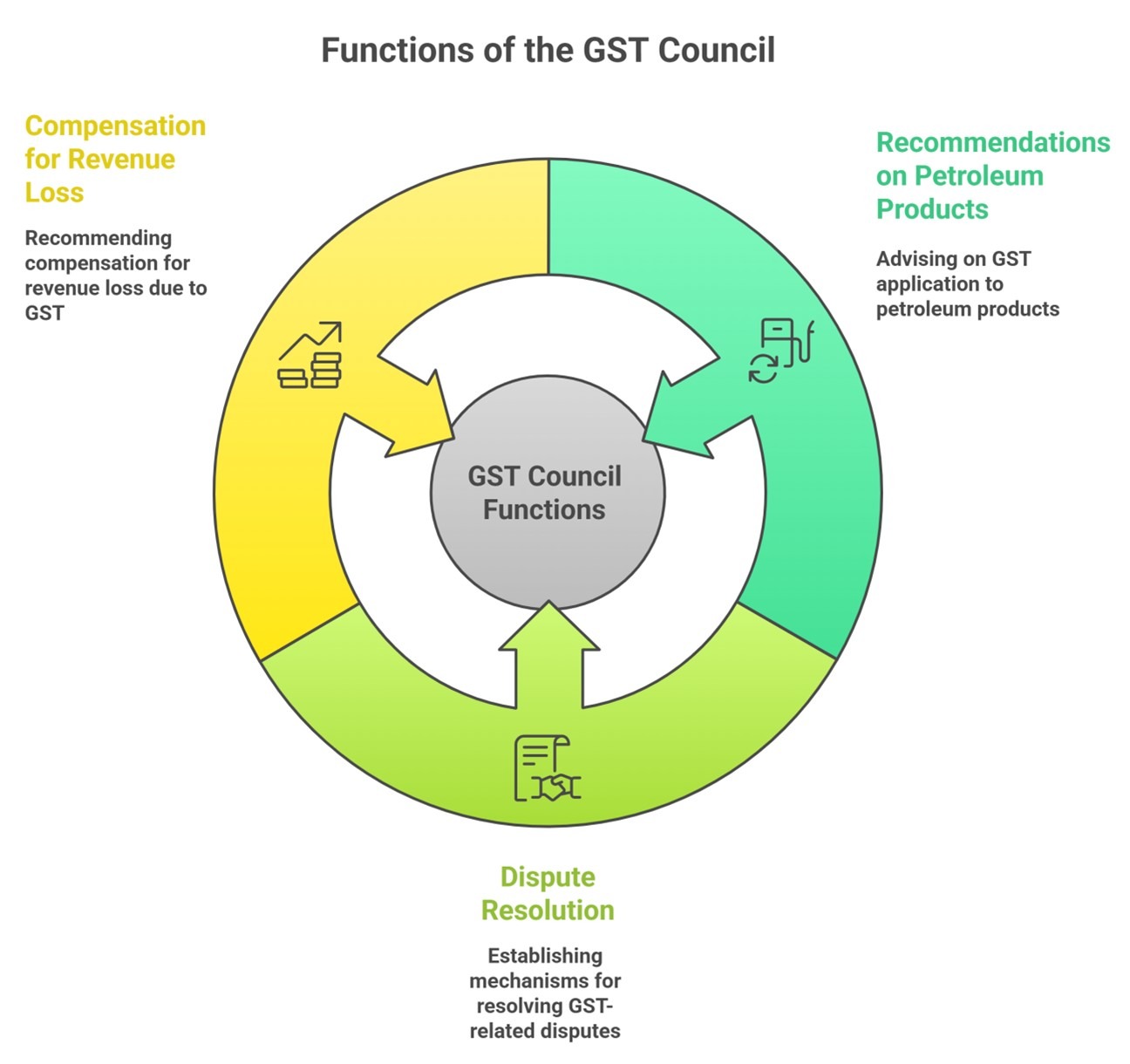

Other Functions of the GST Council

In addition to its primary functions, the GST Council has several supplementary roles:

1. Recommendations on Petroleum Products:

- Recommending when GST may be levied on products like petroleum crude, high-speed diesel, motor spirit (petrol), natural gas, and aviation turbine fuel.

2. Dispute Resolution:

- Establishing a mechanism for adjudicating disputes regarding its recommendations or their implementation, which may involve:

- Disputes between the Centre and one or more states.

- Disputes between the Centre and any state or states against one or more other states.

- Disputes among two or more states.

- Establishing a mechanism for adjudicating disputes regarding its recommendations or their implementation, which may involve:

3. Compensation for Revenue Loss:

Recommending compensation to states for any loss of revenue resulting from the introduction of GST for up to five years. The Parliament determines this compensation based on the recommendations of the Council. Subsequently, the Parliament enacted the relevant law in 2017.

The GST Council is a vital constitutional body that facilitates the smooth implementation of the Goods and Services Tax system in India. Its collaborative nature, grounded in cooperative federalism, ensures that both the Centre and the states participate actively in the tax structure, laying the foundation for a comprehensive and harmonized national market. Proper functioning of the Council helps in addressing issues related to taxation while considering regional and economic diversity.