Evolution of Money

Money is a complex and abstract concept that goes beyond its traditional role as a medium of exchange. It takes on various forms, functions, and characteristics, serving as a societal tool with significant implications for social and cultural dynamics. The evolution of money can be categorized into several stages:

Barter System (Pre-Money): In early human societies, individuals relied on barter to trade goods and services directly, without the use of a standardized medium of exchange. While this system worked effectively on a small scale, it faced significant challenges: inefficiencies hindered transactions, there was a lack of divisibility for certain goods, and the “double coincidence of wants” was a major limitation, as both parties had to want what the other had to offer in order for a trade to occur.

Commodity Money: To address the limitations of barter, societies began to use commodities with intrinsic value as mediums of exchange. Items such as salt, cattle, shells, and precious metals like gold and silver became early forms of money. These commodities were valued for their durability, divisibility, and inherent worth, making them effective tools for facilitating trade and simplifying transactions.

Metallic Coins: As trade progressed, the use of precious metals transitioned into the minting of metallic coins. Governments and rulers began producing standardized coins to guarantee consistency in weight and purity. This advancement created a more convenient and widely accepted medium of exchange, facilitating commerce and enhancing the efficiency of transactions across larger markets.

Representative Money: To overcome the difficulties associated with transporting large quantities of coins, representative money was introduced. This form of money included promissory notes or certificates that could be exchanged for a specific amount of a commodity, such as gold or silver, that was held in reserve. Representative money made transactions more manageable and convenient, allowing people to conduct trade without the need to carry heavy coins.

Paper or Fiat Money: Over time, governments shifted from commodity-backed money to fiat money, which is not tied to a physical commodity but gains its value from public trust and confidence. Fiat currencies are designated as legal tender by governments and are widely accepted for transactions. In India, for example, the Government issues all coins and ₹1 notes under the Coinage Act of 1909, while the Reserve Bank of India (RBI) is empowered by the RBI Act of 1934 to issue the remaining banknotes. This transition to fiat money has allowed for greater flexibility in monetary policy and economic management.

Banknotes and Fractional Reserve Banking (FRB): The rise of banking institutions led to the issuance of banknotes, which represent a claim on a commodity, originally gold or silver. Fractional reserve banking enables banks to lend out more money than they actually hold in reserves, thereby expanding the money supply. This process stimulates the economy by freeing up capital for lending, allowing for increased investment and consumption. Through this mechanism, banks play a crucial role in promoting economic growth and stability.

Electronic and Digital Money: The 20th century heralded the advent of electronic money, starting with the introduction of checks and credit cards. The rise of the internet and technological advancements opened the door to digital currencies and electronic transactions, significantly decreasing the reliance on physical cash. Notable examples include the Digital Ruble in Russia and the eRupee introduced by the Reserve Bank of India (RBI), illustrating the shift towards more convenient and efficient payment methods in today’s economy.

Cryptocurrencies: The 21st century has witnessed the rise of cryptocurrencies, with Bitcoin pioneering this movement. These decentralized digital currencies utilize cryptography for security and are built on blockchain technology, providing a new form of money that challenges the conventions of traditional financial systems. Cryptocurrencies offer unique advantages such as increased transparency, reduced transaction costs, and enhanced accessibility, while also raising new questions about regulation and the future of monetary policy.

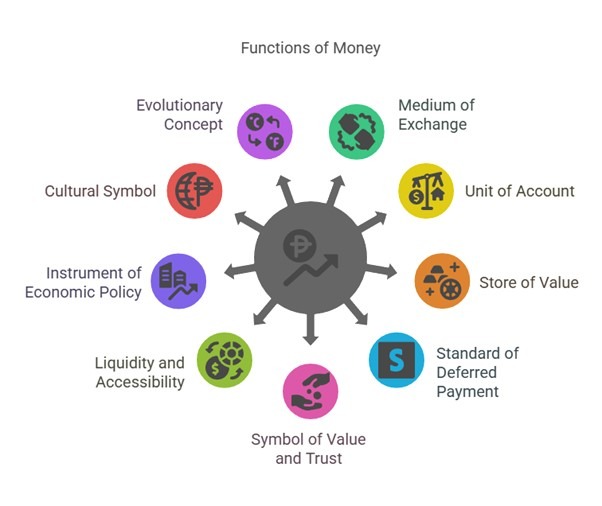

Functions of Money

Medium of Exchange: Money functions as a universally accepted medium that allows individuals and entities to facilitate the exchange of goods, services, or assets. This role enhances transactional efficiency by eliminating the complexities of barter, making it easier for parties to trade and transact in the economy.

Unit of Account: Money serves as a standardized unit of measurement for valuing goods, services, and assets. This function enables a common framework for economic transactions, allowing individuals and businesses to assess, compare, and allocate resources effectively.

Store of Value: Money functions as a repository of wealth, enabling individuals to save and preserve economic value for future use. It serves as a durable and transferable asset over time, allowing people to maintain their purchasing power and invest in future opportunities.

Standard of Deferred Payment: Money facilitates agreements for future transactions by acting as a reliable medium for deferred payments and contractual obligations. This function allows parties to make commitments for payments that will occur at a later date, providing a clear framework for settling debts and fulfilling agreements over time.

Symbol of Value and Trust: Money serves as a symbolic representation of value and trust within a society, reflecting collective beliefs, economic stability, and confidence in the integrity of the financial system. Its acceptance and use are rooted in societal faith in its worth, making it a fundamental cornerstone of economic interactions.

Liquidity and Accessibility: Money is characterized by high liquidity, meaning it can be quickly and easily converted into goods, services, or other assets. This feature provides individuals with flexibility and ready access to resources, allowing them to respond swiftly to their economic needs and opportunities.

Instrument of Economic Policy: Money serves as a crucial tool for governments and central banks in implementing monetary policies. Through the management of money supply and interest rates, these institutions can influence inflation, promote economic growth, and maintain overall economic stability, shaping the financial environment in which businesses and consumers operate.

Cultural Symbol: Beyond its economic functions, money often carries cultural significance, reflecting the historical, political, and social facets of a community. The designs and symbols on currency can encapsulate a nation’s identity and heritage, serving as a representation of shared values, cultural narratives, and national pride among its people.

Evolutionary Concept: Money evolves over time, adapting to technological advancements and changes in societal structures. It has transitioned from traditional physical forms such as coins and banknotes to encompass digital and virtual currencies. This evolution allows money to meet the ever-changing demands of a dynamic world, facilitating efficient transactions in an increasingly digital economy.

Exchange rates

Exchange rates indeed play a significant role in international economics by determining how much of one currency is needed to purchase a unit of another currency. This affects international trade, investment decisions, and overall economic relations between countries.

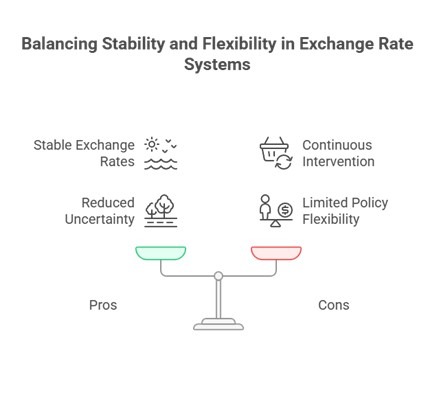

The Fixed Exchange Rate System operates as follows:

- Pegged Value: A country’s currency is fixed at a set rate against another currency or a select group of currencies, ensuring stable exchange rates.

- Intervention Required: To maintain this fixed rate, governments or central banks actively intervene in the foreign exchange market. This involves buying or selling their own currency to offset fluctuations.

- Pros:

- Stability: Provides consistent exchange rates, making international trade and investment more predictable.

- Pros:

- Reduced Uncertainty: Businesses and investors benefit from reduced risk of sudden currency fluctuations.

- Cons:

- Continuous Intervention: Requires frequent intervention in the currency market, which can be resource-intensive.

- Cons:

- Limited Monetary Policy Flexibility: Limits a country’s ability to adjust its own monetary policy as needed to address domestic economic conditions, since maintaining the peg is the priority.

This system emphasizes stability and predictability over flexibility, impacting how nations engage economically both internally and globally.

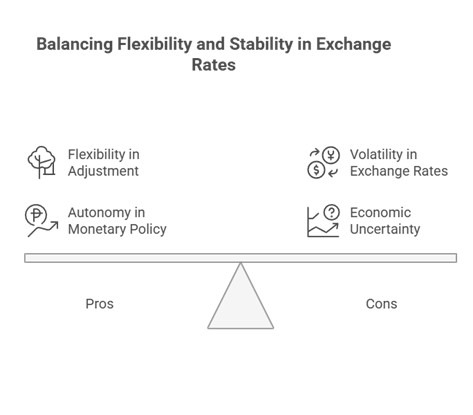

The Floating Exchange Rate System functions with the following characteristics:

- Market-Driven: The value of a currency is primarily determined by supply and demand in the foreign exchange market. This means that a currency will strengthen if demand for it increases or if its supply decreases, and vice versa.

-

- No Fixed Rate: Unlike fixed systems, currency values fluctuate freely, adjusting according to market conditions and economic indicators, such as inflation rates, interest rates, and economic performance.

- Pros:

- Flexibility: Allows for automatic adjustment of currency values in response to external economic factors, which can help countries absorb and adapt to economic shocks

- Pros:

.

- Autonomy: Countries retain greater control over domestic monetary policy since they do not need to maintain a currency peg.

- Cons:

- Volatility: Exchange rates can change rapidly, leading to potential uncertainty in international trade and investment.

- Cons:

- Economic Uncertainty: Businesses and governments may face challenges in budgeting and financial planning due to unpredictable currency movements.

The floating exchange rate system provides a dynamic and responsive way to manage economic conditions, though it comes with the challenge of managing possible instability and unpredictability in exchange rates.

Evolution of Exchange Rate System in India

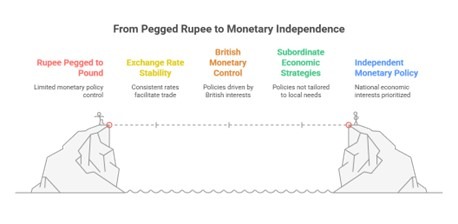

Pre-Independence Era

During the Pre-Independence Era under British colonial rule, the Indian rupee was pegged to the British pound sterling. This arrangement had several implications:

- Exchange Rate Stability: By tying the rupee’s value to the pound, India benefited from consistent and predictable exchange rates, facilitating trade with Britain and its colonies.

-

- Monetary Control: The exchange rate system was controlled by British economic policies, leaving India with little to no autonomy over its own monetary policy. Decisions about currency valuation and economic adjustments were primarily driven by British interests.

-

- Economic Impact: While the stability supported trade with Britain, it also meant that India’s economic strategies and policies were largely subordinate to those of the British economy, limiting the ability to tailor policies to local economic conditions or developmental needs.

This period set the stage for post-independence economic policy development, as India sought to establish greater monetary independence and restructure its financial systems in line with national interests.

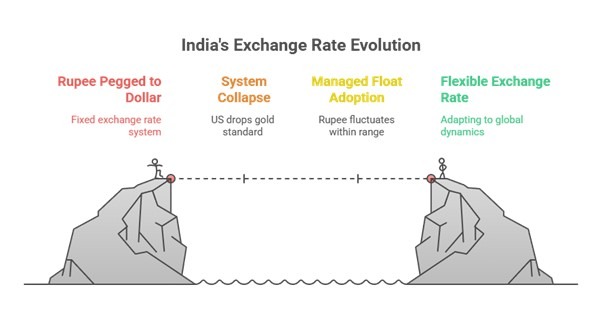

Bretton Woods System (1944-1971):

During the Bretton Woods System period from 1944 to 1971, India was part of a global agreement that established fixed exchange rates with currencies pegged to the U.S. dollar, which was convertible to gold. For India:

- Peg to the U.S. Dollar: The Indian rupee was pegged to the U.S. dollar, providing stability and facilitating international trade under a system designed to encourage economic cooperation and reconstruction post-World War II.

-

- Fixed Exchange Rate Benefits: This arrangement offered the benefits of stable exchange rates, aiding in planning and trade with major global economies.

-

- Collapse in 1971: The system ended when the U.S. dropped the gold standard, effectively dismantling the fixed exchange rate regime as the dollar’s convertibility into gold was suspended, leading to more flexible exchange systems globally.

-

- Transition to Managed Float: Post-1971, India adopted a managed float system, where the rupee was allowed to fluctuate within a specified range, and the Reserve Bank of India (RBI) intervened as needed to stabilize the currency and address economic needs.

This transition marked a shift towards greater flexibility in managing India’s exchange rate, allowing more room for domestic economic policy-making and adaptation to global financial dynamics.

Cryptocurrency

- Cryptocurrencies are a form of digital or virtual currency that utilizes cryptography for security. They operate on decentralized networks and leverage blockchain technology to facilitate secure transactions.

Key Features of Cryptocurrencies:

1. Digital and Virtual Nature:

- Cryptocurrencies exist only in digital form and do not have a physical counterpart, unlike traditional currencies.

2. Cryptography for Security:

- Cryptographic techniques safeguard transactions and control the creation of new units, ensuring the integrity and security of the cryptocurrency.

3. Decentralized Network:

- Cryptocurrencies operate on a decentralized network, meaning that no central authority or institution (like a bank or government) manages them. This decentralization often enhances security and reduces the risk of manipulation or fraud.

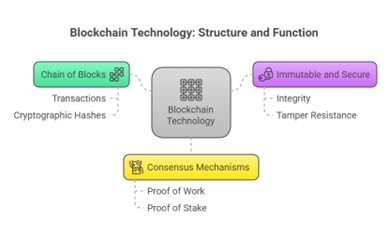

Blockchain Technology

- Blockchain is the underlying technology that powers most cryptocurrencies. It is a distributed and decentralized ledger that records all transactions across a network of computers. Here’s how it works:

1. Chain of Blocks:

- A blockchain is composed of a series of blocks, where each block contains a list of transactions. Each block is linked to the previous one using cryptographic hashes, forming a continuous chain.

2. Immutable and Secure:

- Once a block is added to the blockchain, it cannot be altered retroactively without changing all subsequent blocks. This feature ensures the integrity of the blockchain and makes it resistant to tampering.

3. Consensus Mechanisms:

- Blockchains typically use consensus mechanisms (like Proof of Work or Proof of Stake) to validate transactions and add new blocks to the chain. This ensures that all participants agree on the state of the ledger without a central authority.

Notable Cryptocurrencies

- Bitcoin: Created in 2009, Bitcoin was the first cryptocurrency and remains the most well-known. It introduced the concept of decentralized digital currency to the world.

- Altcoins: Following Bitcoin, many other cryptocurrencies (often referred to as altcoins) have been developed, including Ether (Ethereum), Ripple (XRP), Litecoin, and many more. Each of these may have unique features, use cases, or technologies.

Advantages of Cryptocurrencies

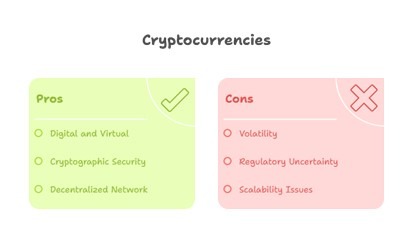

- Decentralization: Reduces reliance on traditional financial institutions and enables peer-to-peer transactions.

- Transparency: Transactions are recorded on a public ledger, promoting accountability and trust.

- Immutability: Once recorded, transactions cannot be altered, ensuring accurate records.

- Security: Use of cryptographic techniques provides a high level of security against fraud and cyberattacks.

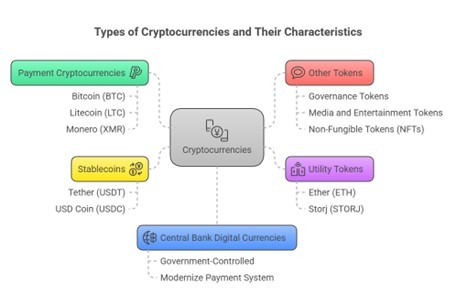

Types of Cryptocurrencies

- The cryptocurrency landscape has evolved into a diverse ecosystem with numerous types of cryptocurrencies, each serving different purposes. Here’s an overview categorizing them into four main types:

1. Payment Cryptocurrencies

- Definition: These are digital currencies designed primarily for peer-to-peer electronic cash transactions.

-

- Characteristics:

- Dedicated blockchains that support general-purpose currency functions.

- Typically do not support smart contracts or decentralized applications (DApps).

- Characteristics:

-

- Notable Examples:

- Bitcoin (BTC): The first and most well-known cryptocurrency, primarily used for transactions.

- Litecoin (LTC): Designed for fast transactions and lower fees.

- Monero (XMR): Focuses on privacy and anonymity in transactions.

- Notable Examples:

-

- Dogecoin (DOGE): Originated as a meme but has gained popularity for tipping and donations.

-

- Bitcoin Cash (BCH): A fork of Bitcoin aimed at increasing transaction speeds and lowering fees.

2. Utility Tokens

- Definition: Tokens that operate on existing blockchains and are used to access specific functions or services within a platform.

-

- Characteristics:

- Facilitate smart contracts and DApps.

- Typically inflationary, with their value influenced by token creation.

- Characteristics:

-

- Notable Examples:

- Ether (ETH): Used for transaction fees and computational services on the Ethereum blockchain.

- Storj (STORJ): Used for decentralized storage services within the Storj network.

- Notable Examples:

3. Stablecoins

- Definition: Cryptocurrencies designed to maintain a stable value by being pegged to fiat currencies like the U.S. dollar or Euro.

- Characteristics:

- Meant to reduce price volatility, providing a reliable store of value and medium of exchange.

- Often backed by reserves to support their value.

- Characteristics:

- Notable Examples:

- Tether (USDT): Pegged to the U.S. dollar and widely used for trading and transactions.

- USD Coin (USDC): Another fiat-backed stablecoin that maintains a stable value.

- Notable Examples:

4. Central Bank Digital Currencies (CBDC)

- Definition: Digital currencies issued by central banks, representing official digital versions of a country’s currency.

-

- Characteristics:

- Typically pegged to domestic currencies, offering increased efficiency for transactions.

- Government-controlled, thus lacking the decentralization and pseudonymity found in other cryptocurrencies.

- Characteristics:

- Significance: CBDCs aim to modernize the payment system, providing a stable digital payment mechanism.

5. Other Tokens

- Governance Tokens: Used for voting and governance in decentralized networks; holders can influence decisions within the protocol.

-

- Media and Entertainment Tokens: Tokens that facilitate transactions in areas such as content consumption, gaming, and online gambling. For example, Basic Attention Token (BAT) rewards users for viewing advertisements.

-

- Non-Fungible Tokens (NFTs): Unique digital assets that represent ownership of distinct items or content, often linked to digital art and collectibles. NFTs differ from typical cryptocurrencies due to their uniqueness and indivisibility.

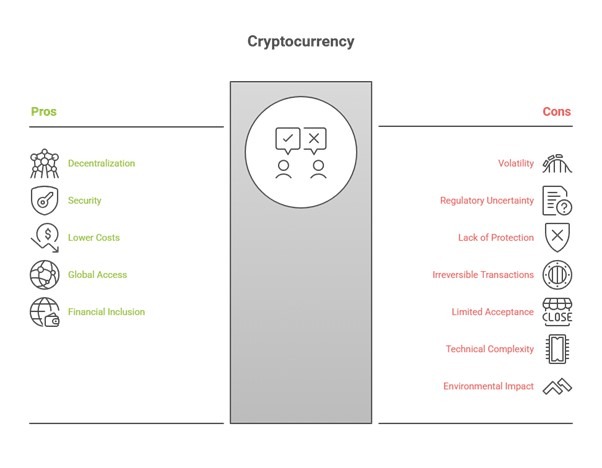

Pros and Cons of Cryptocurrency

- Cryptocurrencies present both advantages and disadvantages that users and investors should carefully consider. Below is a summary of the key pros and cons:

Pros

1. Decentralization:

- Cryptocurrencies operate on decentralized networks, reducing control by any single authority, such as a government or financial institution. This limits the risk of manipulation or interference.

2. Security:

- The use of cryptography ensures secure transactions, making it difficult for unauthorized parties to alter transaction data or engage in fraudulent activities.

3. Lower Transaction Costs:

- Traditional financial systems often involve intermediaries (like banks) that charge fees for their services. Cryptocurrencies can reduce transaction costs by eliminating the need for these intermediaries in many cases.

4. Global Accessibility:

- Cryptocurrencies can be accessed and used by anyone with an internet connection, irrespective of geographical location. This is crucial for individuals in regions with limited access to conventional banking services.

5. Financial Inclusion:

- Cryptocurrencies can provide financial services to unbanked or underbanked individuals, allowing them access to the global financial system and helping to bridge economic disparities.

6. 24/7 Availability:

- Cryptocurrency transactions can occur at any time of day, unlike traditional banking systems that may have limited operating hours.

Cons

1. Volatility:

- Cryptocurrency prices can exhibit significant volatility, leading to large fluctuations in value over short periods. This volatility poses risks for investors and may make cryptocurrencies less suitable for stable financial applications.

2. Regulatory Uncertainty:

- The regulatory environment for cryptocurrencies is still developing in many jurisdictions. Uncertainty regarding government regulations or taxation can create challenges for users and businesses in the sector.

3. Lack of Consumer Protection:

- Unlike traditional financial systems, cryptocurrencies often lack consumer protection schemes. Users may not have recourse for recovering lost funds in cases of fraud or if they lose access to their wallets.

4. Irreversibility of Transactions:

- Once a cryptocurrency transaction is confirmed, it is generally irreversible. This absence of a chargeback mechanism can create challenges in cases of accidental transactions or fraud.

5. Limited Acceptance:

- While adoption is growing, cryptocurrencies are not universally accepted as payment methods. Limited acceptance can restrict their practical use for everyday transactions.

6. Technical Complexity:

- Engaging with cryptocurrencies requires understanding concepts such as private keys, wallets, and blockchain technology, which can be challenging for some users, especially those not tech-savvy.

7. Environmental Concerns:

- The high energy consumption associated with cryptocurrency mining, particularly in proof-of-work systems like Bitcoin, raises environmental concerns related to carbon footprints and ecological sustainability.

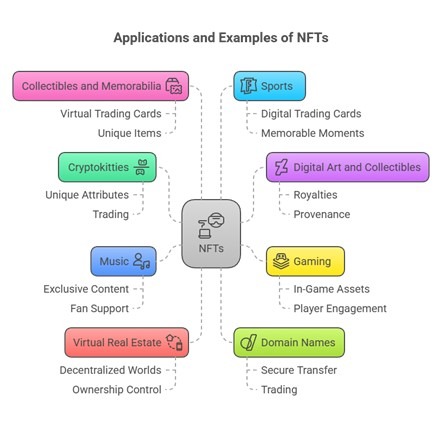

Examples and Uses of NFTs

- Non-fungible tokens (NFTs) have emerged as a transformative technology across various industries, demonstrating their versatility and unique properties. Here are some notable applications and examples of NFTs:

1. Cryptokitties:

- Launched in November 2017, Cryptokitties are one of the first popular uses of NFTs. Each digital cat has unique attributes and identification on the Ethereum blockchain, and they can “reproduce” to create new kittens with various characteristics. Players can buy, sell, and trade these digital cats, highlighting how NFTs can represent ownership of unique digital assets in gaming.

2. Digital Art and Collectibles:

- NFTs gained significant recognition in the art world, allowing digital artists to tokenize their work, thereby establishing ownership and provenance. Artists can sell digital paintings, illustrations, and other forms of digital art as NFTs. This ensures that artists receive royalties on secondary sales, revolutionizing the traditional art market.

3. Gaming:

- In the gaming industry, NFTs represent in-game assets such as characters, skins, weapons, and other virtual items. Players can buy, sell, and trade these assets, often allowing them to move assets between games or platforms. The ownership of these NFTs can enhance player engagement and investment in virtual worlds.

4. Music:

- Musicians can create NFTs for their music, allowing fans to own a piece of their favorite artist’s work. NFTs can grant special access, rewards, or experiences for token holders, such as exclusive content or backstage passes. This provides a new revenue stream for artists and fosters direct support from fans.

5. Virtual Real Estate:

- NFTs are used to represent ownership of virtual land and properties in decentralized virtual worlds, such as Decentraland or Cryptovoxels. Users can buy, sell, and trade virtual real estate as NFTs, which grants them ownership and control over these digital spaces.

6. Domain Names:

- NFTs can represent ownership of domain names on the blockchain. This decentralized approach allows for secure transfer and trading of domain names, reducing reliance on traditional centralized registrars.

7. Collectibles and Memorabilia:

- Beyond digital art, various digital collectibles, such as virtual trading cards or unique virtual items tied to specific events, can be tokenized as NFTs. Collectors can showcase, trade, or sell these tokens, similar to physical collectibles.

8. Sports:

- The sports industry has embraced NFTs by tokenizing sports-related content, such as digital trading cards featuring athletes, memorable moments, and virtual merchandise associated with teams and events. Platforms like NBA Top Shot enable users to buy, sell, and trade highlight moments as collectible NFTs.