Monetary Policy

Monetary policy refers to the strategies and actions implemented by a country’s central bank to regulate the money supply and interest rates within the economy. The primary objectives of monetary policy typically include controlling inflation, fostering economic growth, and maintaining liquidity in the financial system. In India, the Reserve Bank of India (RBI) is responsible for formulating and implementing monetary policy under the Reserve Bank of India Act, 1934.

Objectives of Monetary Policy

1. Control Inflation: One of the key goals is to maintain price stability by controlling inflation, ensuring that the purchasing power of the currency is preserved.

2. Promote Economic Growth: Monetary policy aims to support economic growth by managing the availability and cost of credit, encouraging investment and consumption.

3. Ensure Liquidity: The policy seeks to ensure that there is sufficient liquidity in the economy to facilitate smooth financial transactions and economic activities.

Tools of Monetary Policy

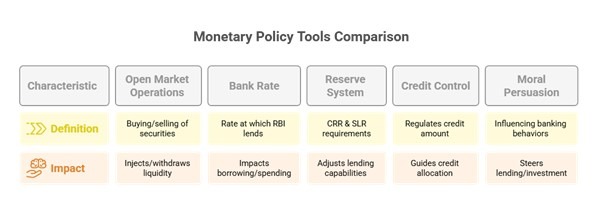

The RBI employs several tools to implement monetary policy effectively:

1. Open Market Operations (OMO):

- The buying and selling of government securities in the open market to regulate the money supply. Buying securities injects liquidity into the economy, while selling them withdraws liquidity.

2. Bank Rate:

- The interest rate at which the RBI lends money to commercial banks. Changes in the bank rate influence other interest rates in the economy, impacting borrowing and spending.

3. Reserve System:

- This includes the Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR):

- CRR: The percentage of a bank’s total deposits that must be held as reserves in cash with the RBI. Increasing the CRR reduces the funds available for lending, while decreasing it provides more credit.

- SLR: The minimum percentage of net demand and time liabilities that banks must maintain in the form of liquid assets. Adjustments to the SLR influence the amount of money banks can lend.

- This includes the Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR):

4. Credit Control:

- Techniques aimed at regulating the amount of credit available in the economy. This includes measures like selective credit control, where the RBI guides credit flow to specific sectors.

5. Moral Persuasion:

- The RBI may use persuasive strategies to influence banking institutions’ lending and investment behaviors without resorting to formal regulations or sanctions.

Evolution of Monetary Policy in India

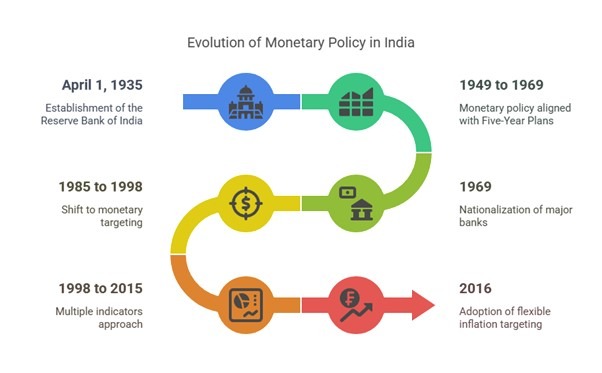

The evolution of monetary policy in India has undergone significant changes since the establishment of the Reserve Bank of India (RBI) in 1935. According to Shri Shaktikanta Das, Governor of the RBI, the evolution can be categorized into seven distinct phases:

1. 1935 to 1949: Initial Phase of RBI

Foundation

- The Reserve Bank of India (RBI) was established on April 1, 1935, during a period marked by the Great Depression. This global economic turmoil significantly influenced the economic environment in which the RBI was founded, prompting the need for a central monetary authority to stabilize and regulate India’s financial system.

Monetary Policy Framework

- The early monetary policy framework of the RBI was guided by the Preamble to the Reserve Bank of India Act, 1934. The primary emphasis during this phase was on maintaining the sterling parity, which aimed to link the value of the Indian currency to the British pound.

Instruments Used

- To effectively regulate liquidity in the economy and manage monetary stability, the RBI employed the following instruments:

- Open Market Operations (OMOs): The buying and selling of government securities to control money supply and influence interest rates.

- Bank Rates: The rate at which the RBI lends money to commercial banks, affecting the cost of borrowing throughout the economy.

- Cash Reserve Ratio (CRR): The percentage of deposits that commercial banks were required to hold as reserves with the RBI, influencing the amount of money available for lending.

- To effectively regulate liquidity in the economy and manage monetary stability, the RBI employed the following instruments:

Limitations

- The period was marked by significant challenges, as the unsettled international monetary system limited the RBI’s policy options. Fluctuations in global economic conditions and the absence of stability in foreign exchange markets constrained the effectiveness of the RBI’s monetary policy tools.

2. 1949 to 1969: Monetary Policy Aligned with Five-Year Plans

Post-Independence Alignment

- Following India’s independence in 1947, the Reserve Bank of India (RBI) adapted its monetary policy to align with the goals of the country’s Five-Year Plans. These plans aimed to promote economic development and growth, emphasizing the need for structured financial support to various sectors of the economy.

Instruments of Policy

- During this period, the RBI deployed several key instruments to implement its monetary policy effectively:

- Bank Rates: The RBI adjusted bank rates to influence borrowing costs for commercial banks, thereby affecting the overall credit availability in the economy.

- Reserve Requirements: The Reserve Bank set mandatory requirements for commercial banks, which dictated the amount of funds banks needed to hold in reserve, influencing their lending capabilities.

- Open Market Operations (OMOs): The RBI conducted OMOs to manage liquidity in the financial system by buying and selling government securities as needed.

- Statutory Liquidity Ratio (SLR): Introduced during this period, SLR required banks to maintain a specified percentage of their net demand and time liabilities in liquid assets, thus supporting government borrowing and ensuring liquidity.

- During this period, the RBI deployed several key instruments to implement its monetary policy effectively:

Directed Credit

- A significant focus of monetary policy during this era was on directing credit to priority sectors such as agriculture, small industries, and other developmental activities. This strategy aimed to foster economic growth and ensure that essential sectors received adequate funding.

- While there was a strong focus on supporting targeted sectors, the emphasis on price stability became relatively secondary during this period. The priority was to stimulate growth and development, often leading to increased credit allocation to specified industries without stringent controls on inflation.

3. 1969 to 1985: Credit Planning

Bank Nationalization

- The nationalization of major banks in 1969 marked a significant shift in the Indian banking landscape. This move aimed to enhance credit availability across various sectors, particularly those deemed essential for national development. By bringing major banks under government control, the objective was to redirect funds toward priority sectors, such as agriculture, small industries, and infrastructure development.

Credit Planning

- Following nationalization, the RBI introduced formal credit planning mechanisms to more effectively allocate financial resources to targeted sectors. Key aspects of this approach included:

- Selective Credit Control: The RBI implemented measures like quantitative restrictions on credit to ensure that specific sectors received adequate funding. This included limiting the amount banks could allocate to certain industries.

- Interest Rate Adjustments: The RBI also adjusted interest rates to influence credit availability, encouraging banks to lend more to priority sectors by making borrowing cheaper.

- Following nationalization, the RBI introduced formal credit planning mechanisms to more effectively allocate financial resources to targeted sectors. Key aspects of this approach included:

Inflationary Pressures

- The period from 1969 to 1985 was characterized by significant inflationary pressures. Several factors contributed to rising inflation:

- Excessive Credit Expansion: The focus on channeling credit toward priority sectors, while sometimes necessary for development, led to an oversupply of money in the economy, contributing to inflation.

- External Shocks: The economy faced several external challenges, including wars and oil crises, which exacerbated inflation. These shocks increased costs for goods and services and put additional strain on the economy.

- The period from 1969 to 1985 was characterized by significant inflationary pressures. Several factors contributed to rising inflation:

4. 1985 to 1998: Monetary Targeting

Fiscal Dominance

- During the 1980s, India experienced a rise in automatic monetization of the budget deficit. This occurred when the government financed its budget deficits by borrowing from the Reserve Bank of India (RBI), leading to an increase in the Statutory Liquidity Ratio (SLR). The reliance on monetary expansion to fund deficits often had implications for overall monetary stability and inflation.

Shift to Monetary Targeting

- In response to the inflationary pressures and economic challenges of the time, there was a shift toward monetary targeting. The focus changed to controlling the money supply and credit aggregates as intermediate targets to effectively manage inflation.

- This involved setting explicit targets for money supply growth and directing monetary policy actions to achieve those targets.

- In response to the inflationary pressures and economic challenges of the time, there was a shift toward monetary targeting. The focus changed to controlling the money supply and credit aggregates as intermediate targets to effectively manage inflation.

Chakravarty Committee Recommendations

- The Chakravarty Committee, constituted in 1985, made significant recommendations aimed at instituting a more structured approach to monetary policy:

- The committee advocated for monetary targeting as a means to limit excessive monetary expansion that contributed to inflation. By strictly controlling the growth of the money supply, it aimed to stabilize prices and curb inflationary expectations.

- The Chakravarty Committee, constituted in 1985, made significant recommendations aimed at instituting a more structured approach to monetary policy:

Challenges

- The period of monetary targeting uncovered notable challenges:

- Unstable Relationship: The relationship between money supply and inflation proved to be unstable in the Indian context. Economic conditions and structural changes often caused disconnects between changes in money supply and observable inflation rates.

- Limitations of the Approach: The limitations of relying solely on monetary targeting became evident as external factors, such as fluctuations in oil prices and domestic economic pressures, complicated the effectiveness of conventional monetary tools.

- The period of monetary targeting uncovered notable challenges:

5. 1998 to 2015: Multiple Indicators Approach

Economic Liberalization

- The liberalization of the Indian economy that began in the early 1990s led to significant structural changes and necessitated a revised approach to monetary policy. As markets opened and economic reforms were implemented, the Reserve Bank of India (RBI) recognized the need for a more dynamic response to the evolving financial landscape.

Expanded Framework

- In response to these changes, the RBI adopted a multiple indicators approach to monetary policy:

- This flexible framework involved considering a broader range of indicators beyond just money supply. Key indicators included:

- Economic Output: Monitoring GDP growth and overall economic activity.

- Credit Levels: Observing the trends in credit flow to various sectors to gauge economic health.

- Inflation Rates: Keeping an eye on inflation metrics to maintain price stability.

- Exchange Rates: Analyzing currency fluctuations to assess external economic factors and their implications on domestic conditions.

- This flexible framework involved considering a broader range of indicators beyond just money supply. Key indicators included:

- This comprehensive approach allowed the RBI to be more responsive to changing economic conditions, making it easier to adjust monetary policy in line with various economic indicators.

- In response to these changes, the RBI adopted a multiple indicators approach to monetary policy:

Outcomes

- The implementation of the multiple indicators approach had notable outcomes:

- Growth Rate: From 1998-99 to 2008-09, India experienced an impressive average domestic growth rate of approximately 6.4%. This growth was attributed to increased credit availability and more effective monetary policy aimed at supporting economic expansion.

- Moderated Inflation: During this period, wholesale price index (WPI) inflation was managed and averaged around 5.4%, reflecting the RBI’s effective monitoring and policy actions to keep inflation within reasonable limits.

- The implementation of the multiple indicators approach had notable outcomes:

6. 2013 to 2016: Preconditions Set for Inflation Targeting

Post-Crisis Responses

- Following the global financial crisis of 2008, India faced significant challenges, including persistent inflation and a slowdown in economic growth. This situation underscored the necessity for a more transparent and effective monetary policy framework to tackle rising inflation while stimulating economic recovery.

Urjit Patel Committee

- In 2014, the Urjit Patel Committee was established to assess the monetary policy framework of India. One of its key recommendations was to adopt inflation targeting as a nominal anchor for monetary policy, suggesting that a clear and defined target for inflation would bring greater stability and predictability to economic conditions.

Inflation Targeting Framework

- The RBI formally adopted the inflation targeting framework in 2016 following the committee’s recommendations. Key features of this framework included:

- Inflation Target: The RBI set a target inflation rate of 4%, with a tolerance band of +/- 2%. This means the RBI aims to maintain inflation within the range of 2% to 6%.

- Prioritization of Price Stability: The framework places a strong emphasis on maintaining price stability as a primary objective of monetary policy. The commitment to controlling inflation is intended to instill confidence among investors and consumers and foster sustainable economic growth.

- The RBI formally adopted the inflation targeting framework in 2016 following the committee’s recommendations. Key features of this framework included:

7. 2016 Onwards: Flexible Inflation Targeting

Amendment of RBI Act

- In May 2016, the Reserve Bank of India Act was amended to formally adopt a framework of flexible inflation targeting. This amendment marked a significant evolution in the RBI’s monetary policy approach, emphasizing the importance of maintaining price stability while also supporting economic growth.

Monetary Policy Framework Agreement

- The Monetary Policy Framework Agreement established a structured commitment for cooperation between the Government of India and the RBI. This agreement clarified the roles and responsibilities of the RBI in monetary policymaking and reinforced its independence in conducting monetary policy.

- This collaboration facilitates effective communication and alignment between fiscal and monetary policy, encouraging a cohesive approach to economic management.

Focus on Stability and Growth

- Under the flexible inflation targeting framework, the RBI actively focuses on achieving the inflation target while also considering the broader necessity for economic growth.

- The RBI employs various monetary policy tools, including:

- Repo Rates: Adjusting the interest rate at which the RBI lends to commercial banks, influencing borrowing costs and liquidity in the economy.

- Open Market Operations (OMOs): Buying and selling government securities to regulate the money supply and control liquidity.

- This dual focus allows the RBI to adapt its policies to changing economic conditions, balancing the need to manage inflation with the imperatives of supporting sustainable economic growth. 407630

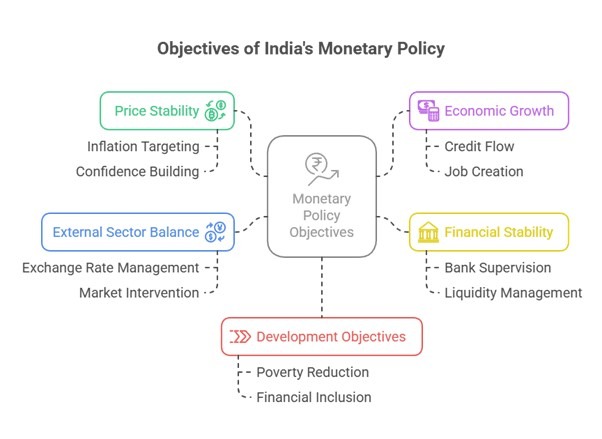

Objectives of India’s Monetary Policy

The objectives of India’s monetary policy are centered around ensuring economic stability, promoting growth, and fostering a conducive environment for sustainable development. The Reserve Bank of India (RBI) strives to achieve these goals through a comprehensive monetary policy framework. Here are the key objectives:

1. Price Stability:

- Importance: Maintaining a stable price level is crucial as it reduces uncertainty for businesses and consumers. Price stability fosters confidence in the economy, encouraging long-term investments and promoting sustainable economic growth.

- Current Framework: The RBI follows a flexible inflation targeting framework, with a target inflation rate of 4% and a tolerance band of +/- 2%, aiming to keep inflation within this range.

2. Economic Growth:

- Stimulation of Activity: Monetary policy tools are employed to stimulate economic activity, facilitating job creation and overall prosperity.

- Credit Flow: The RBI focuses on ensuring an adequate flow of credit to key sectors such as agriculture, industry, and infrastructure, which are essential for driving economic growth and development.

3. Financial Stability:

- Stability of the Financial System: Ensuring a sound and stable financial system is vital for protecting depositors, preventing financial crises, and promoting efficient allocation of resources.

- Regulatory Instruments: The RBI uses various instruments, including bank supervision, regulations, and liquidity management practices, to ensure the stability of banks and other financial institutions.

4. External Sector Balance:

- Exchange Rate Management: Managing the exchange rate and maintaining a balance of payments equilibrium is essential for facilitating international trade and investment while preventing excessive currency volatility.

- Market Intervention: The RBI intervenes in the foreign exchange market when necessary to stabilize the Indian rupee and ensure orderly foreign exchange transactions.

5. Development Objectives:

- Support for Government Goals: Monetary policy plays a significant role in supporting broader government development objectives, including poverty reduction, financial inclusion, and sustainable development.

- Targeted Initiatives: The RBI implements targeted credit schemes and initiatives to promote these goals, ensuring that financial resources contribute to inclusive growth and the development of underprivileged sectors.

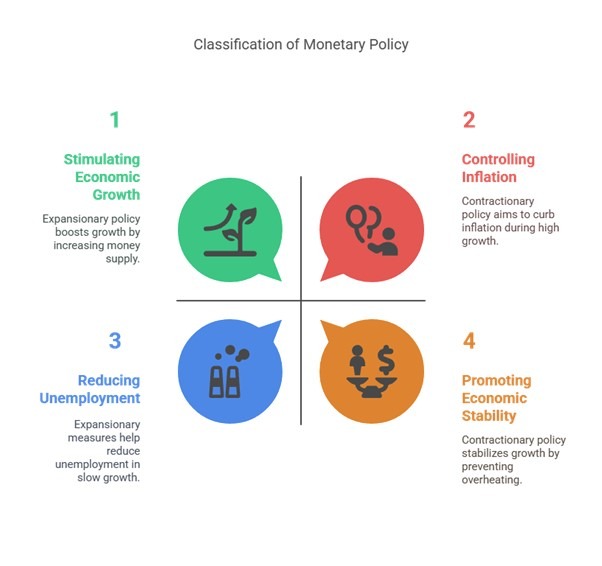

Classification of Monetary Policy

Monetary policy can be classified based on the prevailing economic conditions and the objectives it aims to achieve. The two primary classifications are expansionary monetary policy and contractionary monetary policy.

1. Expansionary Monetary Policy

Definition:

- Often referred to as loose monetary policy, this approach involves increasing the supply of money and credit within an economy.

Objectives:

- Stimulate Economic Growth: The primary aim is to foster economic growth by making money more available to individuals and businesses.

- Reduce Unemployment: During periods of economic downturn or recession, expansionary policy helps alleviate unemployment by encouraging investment and consumption.

Implementation:

- Lowering Interest Rates: The central bank reduces interest rates, making loans more affordable and accessible for borrowers.

- Increasing Money Supply: Through tools such as open market operations, the central bank buys government securities, injecting liquidity into the market.

Expected Outcomes:

- Increased availability of money at lower costs leads to higher consumer spending on goods and services.

- Enhanced business investment as borrowing becomes more attractive, ultimately stimulating economic activity and growth.

2. Contractionary Monetary Policy

Definition:

- Also known as tight or contractionary monetary policy, this approach is employed to curb inflation, particularly when the economy is growing too rapidly (overheating).

Objectives:

- Control Inflation: The primary goal is to decrease the money supply and control inflationary pressures within the economy.

- Promote Economic Stability: By preventing overheating, contractionary policy seeks to maintain a sustainable pace of economic growth.

Implementation:

- Raising Interest Rates: The central bank increases interest rates, making borrowing more expensive and less attractive.

- Decreasing Money Supply: Through tools such as selling government securities in open market operations, the central bank withdraws liquidity from the economy.

Expected Outcomes:

- Higher interest rates discourage borrowing and spending, leading to a decrease in business investments and significant consumer purchases (e.g., houses, cars).

- Reduced consumer spending contributes to stabilizing prices and inflation levels.

Monetary Policy Tools

The Reserve Bank of India (RBI) employs various tools to implement monetary policy effectively, influencing the overall money supply and ensuring financial stability in the economy. These tools can be broadly classified into quantitative measures and qualitative measures. Below, we focus on the quantitative measures used by the RBI.

Quantitative Measures

Quantitative measures involve actions that directly affect the total money supply in the economy. Key instruments under this category include:

1. Bank Rate:

- This is the rate at which the RBI is willing to buy or rediscount bills of exchange and other commercial papers. Changes in the bank rate influence lending rates across various financial institutions.

2. Cash Reserve Ratio (CRR):

- The CRR is the percentage of a bank’s Net Demand and Time Liabilities (NDTL) that must be maintained as reserves with the RBI in cash form. An increase in the CRR reduces the amount of money available for banks to lend, thereby tightening liquidity.

3. Statutory Liquidity Ratio (SLR):

- The SLR is the portion of NDTL that banks must maintain in safe and liquid assets, such as government securities, cash, and gold. Adjusting the SLR affects banks’ lending capacity and ensures that they maintain sufficient liquidity.

4. Liquidity Adjustment Facility (LAF):

- The LAF includes overnight and term repo auctions that help banks manage short-term liquidity mismatches. This facility allows banks to borrow from the RBI against collateralized government securities for overnight liquidity needs.

5. Repo Rate:

- The repo rate is the fixed interest rate at which the RBI provides overnight liquidity to banks, allowing them to borrow funds against collateral of approved securities. A lower repo rate typically encourages banks to borrow more, boosting credit availability in the economy.

6. Reverse Repo Rate:

- The reverse repo rate is the fixed interest rate at which the RBI absorbs liquidity from banks by borrowing funds in exchange for government securities. This tool is used to manage excess liquidity in the banking system.

7. Marginal Standing Facility (MSF):

- The MSF is a facility allowing scheduled commercial banks to borrow additional overnight funds from the RBI at a rate higher than the repo rate. This serves as a safety valve against unforeseen liquidity shocks, helping maintain stability in the banking system.

8. Corridor:

- The corridor refers to the range of movement in the weighted average call money rate, determined by the MSF rate (upper bound) and the reverse repo rate (lower bound). It helps to regulate liquidity conditions and influences interbank lending rates.

9. Market Stabilisation Scheme (MSS):

- Introduced in 2004, the MSS is used to manage surplus liquidity resulting from significant capital inflows by selling short-dated government securities and treasury bills. This helps absorb excess liquidity and maintain stability in the financial markets.

10. Open Market Operations (OMOs):

- OMOs involve the outright purchase and sale of government securities. By buying securities, the RBI injects liquidity into the economy; by selling them, it absorbs liquidity. OMOs are a crucial tool for managing long-term liquidity.