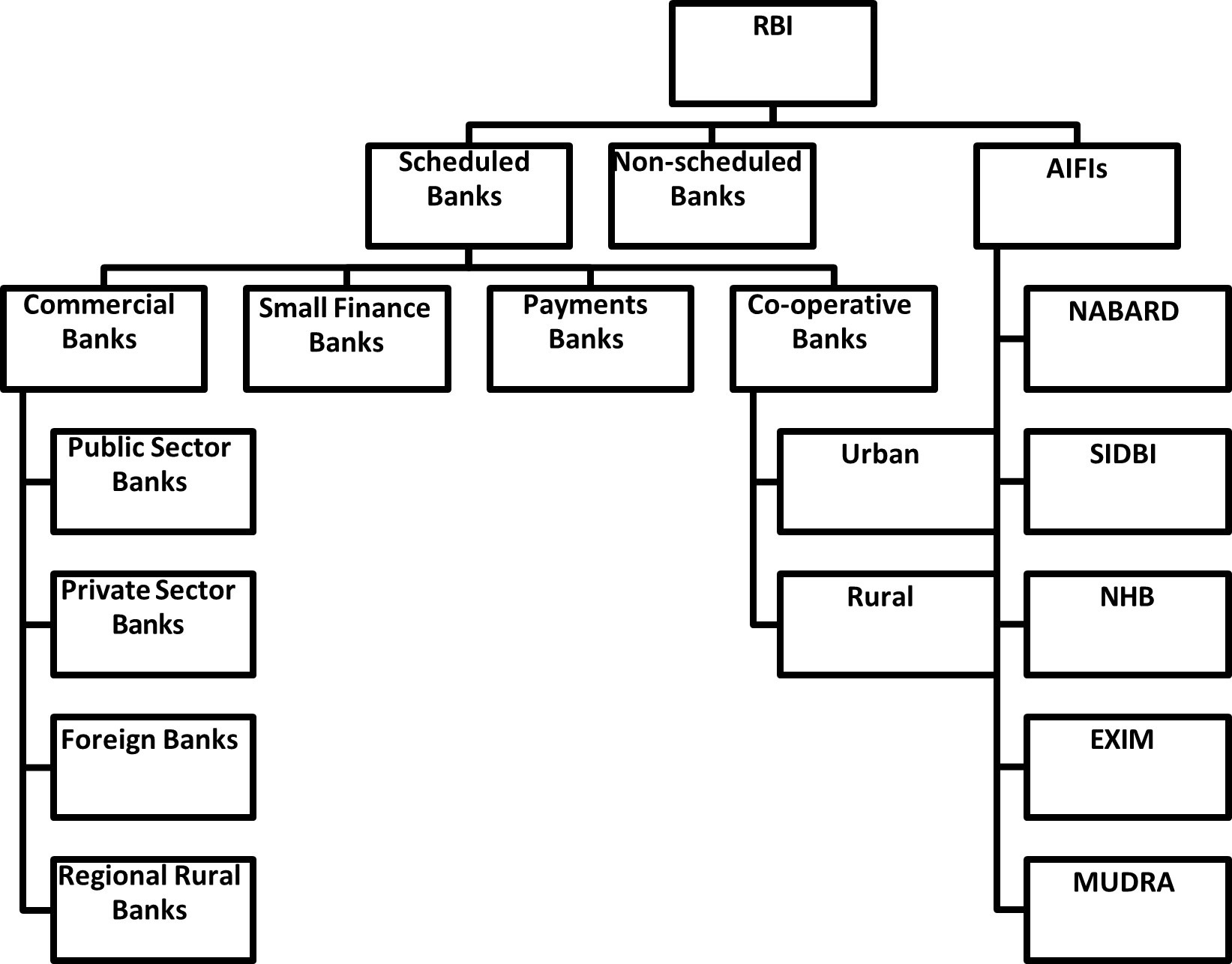

3. Based on Area of Operation

1. Scheduled Banks:

- Listed under the Second Schedule of the RBI Act, 1934.

- Fulfill criteria laid down by the RBI, such as minimum paid-up capital and reserves.

- Enjoy privileges like access to RBI refinancing facilities.

2. Non-Scheduled Banks:

- Not listed in the Second Schedule of the RBI Act.

- Smaller in size and do not enjoy benefits available to scheduled banks.

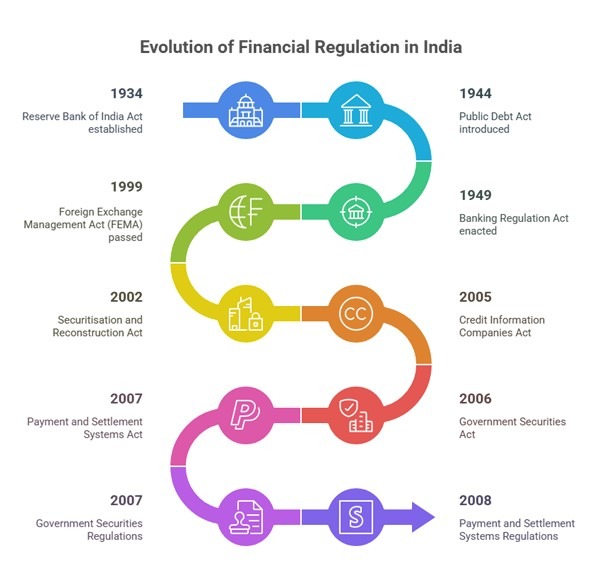

Key Acts Governing the Reserve Bank of India and Financial Regulation

The Reserve Bank of India (RBI) operates under several key legislative frameworks that govern its functions, powers, and the broader financial landscape in India. Below are important acts that play significant roles in regulating various aspects of banking, finance, and economic management:

1. Reserve Bank of India Act, 1934:

- This foundational act established the RBI and outlines its objectives, powers, structure, and functions, including monetary policy formulation and currency issuance.

2. Banking Regulation Act, 1949:

- Provides a comprehensive framework for regulating and supervising commercial banks in India, ensuring stability and soundness within the banking sector.

3. Public Debt Act, 1944 / Government Securities Act, 2006:

- This act allows the government to borrow money through the issuance of government securities, facilitating public debt management.

4. Government Securities Regulations, 2007:

- These regulations govern the issuance and trading of government securities, ensuring orderly functioning in the government securities market.

5. Foreign Exchange Management Act (FEMA), 1999:

- Regulates foreign exchange markets in India, facilitating external trade and payments while promoting the orderly development of the foreign exchange market.

6. Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002:

- This act allows financial institutions to securitize their assets, providing a legal framework for the reconstruction of financial assets and the enforcement of security interests.

7. Credit Information Companies (Regulation) Act, 2005:

- Regulates credit information companies (CICs) to enhance the accuracy of credit information, thereby facilitating responsible lending practices and protecting borrowers’ rights.

8. Payment and Settlement Systems Act, 2007:

- This act provides a regulatory framework for payment systems in India to ensure safe, secure, and efficient payment transactions.

9. Payment and Settlement Systems Act, 2007 (As Amended up to 2019):

- Refers to amendments made to the original legislation that may address emerging payment trends, technologies, and regulatory needs.

10. Payment and Settlement Systems Regulations, 2008 (As Amended up to 2022):

- These regulations set forth specific requirements and guidelines for the operation of various payment systems, ensuring compliance with legislative frameworks.

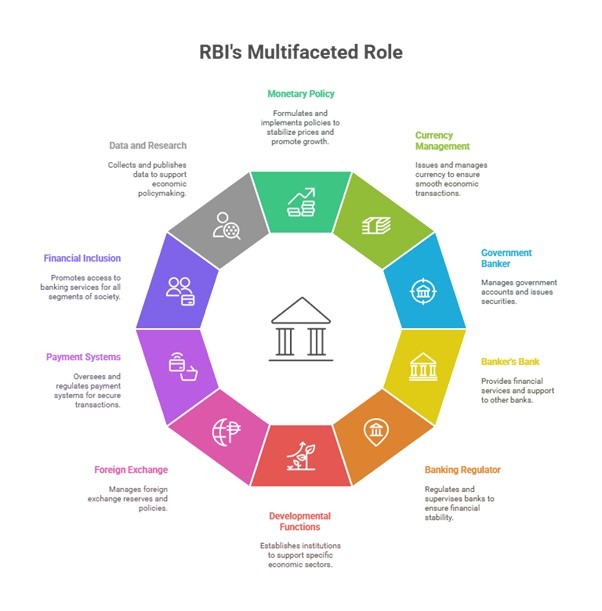

Functions of the Reserve Bank of India (RBI)

The Reserve Bank of India (RBI) plays a pivotal role in the Indian economy by performing several key functions that contribute to monetary stability, financial integrity, and economic development. Below is a comprehensive overview of these functions:

1. Monetary Policy Formulation and Implementation:

- The RBI is responsible for formulating and implementing monetary policy to achieve price stability and promote economic growth.

- Tools Used:

- Repo Rates: The interest rate at which the RBI lends money to commercial banks, influencing overall borrowing costs in the economy.

- Reverse Repo Rates: The rate at which banks can deposit excess funds with the RBI, affecting liquidity in the banking system.

- Open Market Operations: The buying and selling of government securities to manage the money supply and liquidity in the economy.

2. Currency Issuance and Management:

- The RBI holds the exclusive authority to issue currency notes in India, excluding the one-rupee coin.

- It manages the supply of currency and credit to ensure currency stability, facilitating economic transactions smoothly within the market.

3. Banker to the Government:

- The RBI acts as the banker and financial advisor to the Government of India, managing its accounts and handling the issuance of government securities.

- It conducts all banking transactions for the government, ensuring efficient financial management.

4. Banker’s Bank and Lender of Last Resort:

- The RBI serves as the banker to other banks, maintaining their banking accounts and providing necessary financial services.

- As a lender of last resort, it provides emergency financial support to banks experiencing liquidity crises, thereby maintaining stability in the banking sector.

5. Regulator and Supervisor of the Banking System:

- The RBI regulates and supervises commercial banks and financial institutions to ensure the stability and integrity of the financial system.

- It issues banking licenses, establishes regulatory frameworks, and monitors compliance among financial entities to promote sound banking practices.

6. Developmental Functions:

- The RBI undertakes various developmental roles to foster a robust financial system, such as establishing institutions like the National Housing Bank (NHB) and the National Bank for Agriculture and Rural Development (NABARD) to support specific sectors of the economy.

7. Foreign Exchange Management:

- The RBI manages the country’s foreign exchange reserves, formulating policies to facilitate external trade, payments, and overall financial stability related to foreign currencies.

8. Payment and Settlement Systems:

- The RBI oversees and regulates payment and settlement systems in the country, ensuring that they are efficient, secure, and reliable for economic transactions, contributing to the broader financial infrastructure.

9. Financial Inclusion:

- The RBI promotes financial inclusion by developing policies and initiatives aimed at expanding banking services to unbanked and underprivileged segments of society, enhancing access to financial resources.

10. Data Collection and Research:

- The RBI compiles and publishes data on various economic indicators and conducts research to support economic policymaking. This research aids in informed decision-making for both the RBI and the government.

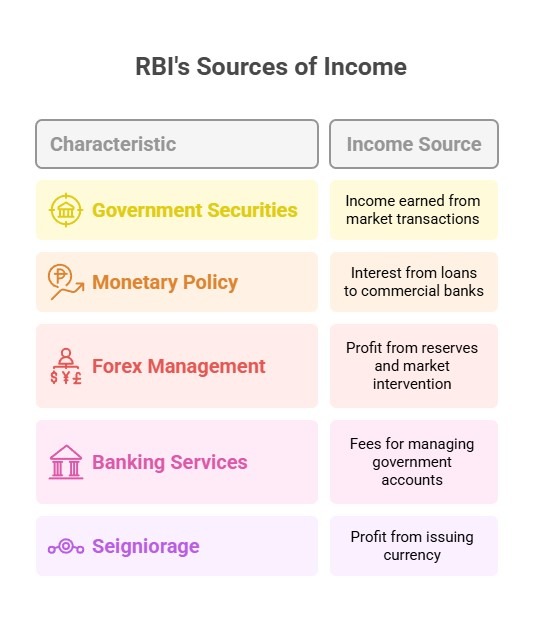

RBI’s Sources of Income

The Reserve Bank of India (RBI) generates revenue through various methods. These income sources are vital for its operations and contribute to its ability to manage monetary policy, regulate the banking sector, and provide financial stability. Here are the key sources of income for the RBI:

1. Purchase and Sale of Government Securities:

- The RBI earns income by buying and selling government securities in the open market. These transactions influence liquidity in the economy and are part of the RBI’s monetary policy operations.

2. Monetary Policy Operations:

- Through mechanisms like the repo market, the RBI provides short-term loans to commercial banks. The interest earned on these loans is a significant source of revenue for the RBI.

3. Foreign Exchange Reserves Management:

- The RBI manages the country’s foreign exchange reserves, which include foreign currencies, gold, and other reserve assets. It generates profit from the appreciation of these assets’ values. Additionally, the RBI earns revenue from its interventions in the foreign exchange market.

4. Banking Services to the Government:

- Acting as the banker to both central and state governments, the RBI charges fees for various services. This includes managing government accounts, handling cash flows, and facilitating the issuance and redemption of government bonds.

5. Seigniorage:

- Seigniorage refers to the profit made by the central bank from issuing currency. It is the difference between the face value of the currency and the cost of producing and distributing it. Seigniorage represents an important source of revenue for the RBI.

-

- After covering its operational expenses and maintaining adequate reserves, the RBI transfers surplus profits, including seigniorage, to the government, contributing to the government’s revenue.

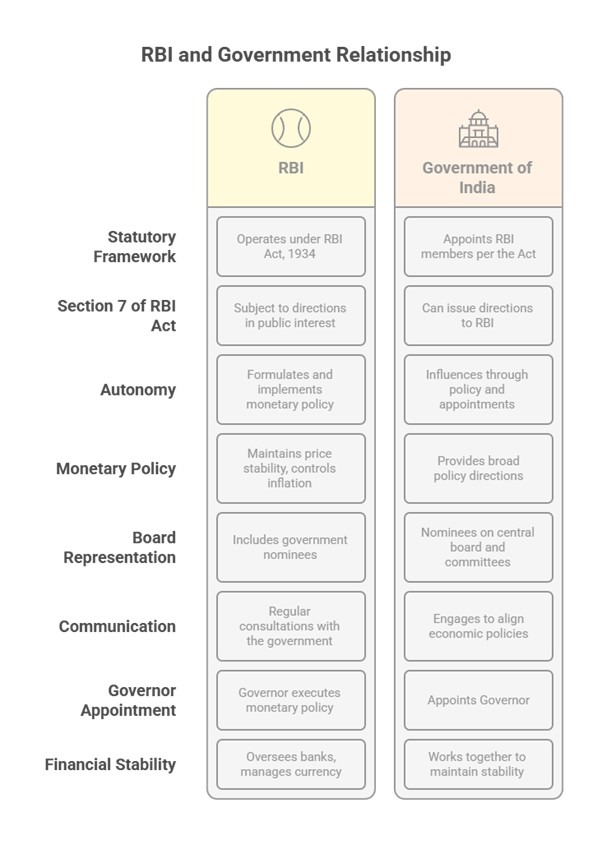

Relationship Between RBI and the Government of India

The relationship between the Reserve Bank of India (RBI) and the Government of India is characterized by a collaboration that balances the central bank’s autonomy with the government’s policy directives. Below are the key aspects of this relationship:

1. Statutory Framework:

- The RBI operates under the framework established by the Reserve Bank of India Act, 1934. This legislation outlines the central bank’s functions, powers, and specifies the relationship between the RBI and the government, including the appointment of RBI members by the government.

2. Section 7 of the Reserve Bank of India Act:

- Section 7 allows the Central Government to issue directions to the RBI after consulting the Governor, as deemed necessary in the public interest.

- Section 7(2) provides the government with the power to entrust operations of the RBI to its board of directors, emphasizing the oversight role the government plays.

3. Autonomy of the Reserve Bank of India:

- The RBI is granted autonomy to formulate and implement monetary policy, which is essential for maintaining price stability and controlling inflation.

- While the central bank operates independently, it is not entirely free from government influence, thus requiring a delicate balance.

4. Monetary Policy Framework:

- The RBI and the government collaborate to establish the monetary policy framework for the country. The RBI’s primary objective is to maintain price stability while also considering economic growth.

- While the government can provide broad policy directions, the RBI has the authority to make specific decisions regarding interest rates, money supply, and other monetary tools.

5. Government Representation on RBI’s Boards:

- The government plays a role in the governance of the RBI through representation on the bank’s central board and committees.

- The central board includes government nominees, thereby allowing for input from the government perspective.

6. Consultations and Communication:

- Regular consultations and communication occur between the government and the RBI to address economic conditions and policy priorities.

- The Finance Ministry engages with the RBI to ensure alignment of economic policies and coordinate responses to emerging challenges.

7. Appointment of the RBI Governor:

- The appointment of the RBI Governor is made by the government, specifically by the Prime Minister in consultation with the Finance Minister.

- The Governor plays a critical role in both formulating and executing monetary policy, making this appointment significant in the context of monetary governance.

8. Coordination on Financial Stability:

- The RBI and the government work together to maintain financial stability in the economy. This includes overseeing banks, managing the currency, and ensuring the overall stability of the financial system.

- Collaborative efforts help in addressing systemic risks and facilitating a resilient financial environment.