Classification of Parliamentary Committees

Parliamentary committees can be broadly classified into two categories:

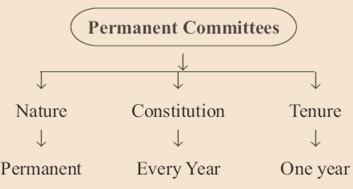

- Standing Committees: These are permanent committees constituted every year or periodically according to the rules of procedure and conduct of business. Their work is of a continuous nature.

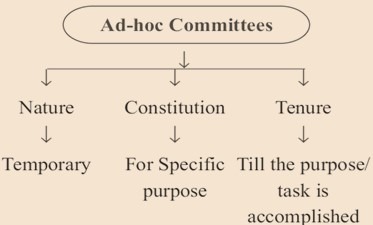

- Ad Hoc Committees: These are temporary committees appointed for a specific purpose, and they cease to exist once they have completed their assigned task and submitted their report. These can be further classified into Enquiry Committees and Advisory Committees.

Committee on Public Undertakings

- Historical Background: It was created in 1964 on the recommendation of the Krishna Menon Committee.

Functions:

- Examination of Reports and Accounts: The committee examines the reports and accounts of public undertakings to ensure financial prudence and effective utilization of resources.

- Accountability of Public Undertakings: It holds public undertakings accountable for their performance and adherence to prescribed norms and guidelines.

- Evaluation of Efficiency and Economy: The committee evaluates the efficiency and economy in the administration of public undertakings, recommending measures for improvement.

- Performance Audit: It conducts a performance audit of selected public undertakings to assess their achievements against predetermined objectives.

- Recommendations for Improvement: Based on its examinations, the committee makes recommendations for enhancing the functioning, profitability, and overall efficiency of public undertakings.

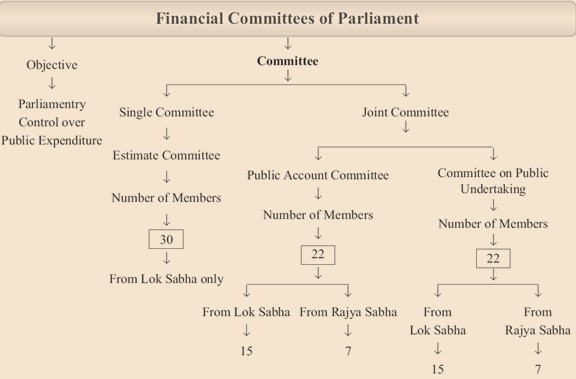

Aspect | Public Accounts Committee (PAC) | Estimates Committee (EC) | Committee on Public Undertakings (COPU) |

Primary Function | Confirms expenditure is made for the designated purpose; checks misappropriation of funds. | Suggests reforms to make public expenditure more prudent and efficient. | Extracts executive accountability via CAG reports on public undertakings. |

Focus Area | Examines public expenditure for waste, loss, and corruption. | Suggests alternative policies to check executive overreach in policymaking. | Ensures PSUs are managed per sound business principles. |

Authority/Power | Can question prudence and wisdom of the executive in using public funds. | Influences policymaking by providing alternatives to the executive. | Examines discretion used in PSU operations and reduces misuse. |

Departmental Standing Committees:

There are 24 such committees, with eight under the Rajya Sabha and 16 under the Lok Sabha. Their functions include:

- To consider the Demands for Grants of the related Ministries/Departments and report thereon to the Houses. This report should not suggest anything of the nature of cut motions.

- To examine Bills pertaining to the related Ministries/Departments as are referred to them by the Chairman or the Speaker and report thereon.

- To consider the Annual Reports of the Ministries/Departments and report thereon.

- To consider national basic long-term policy documents presented to the Houses, if referred to the Committee by the Chairman or the Speaker, and report thereon.

- They do not generally consider matters examined by other parliamentary committees.

- Their recommendations are advisory and not binding on Parliament.

- Each committee follows a procedure for considering the demands for grants and making a report to the Houses.

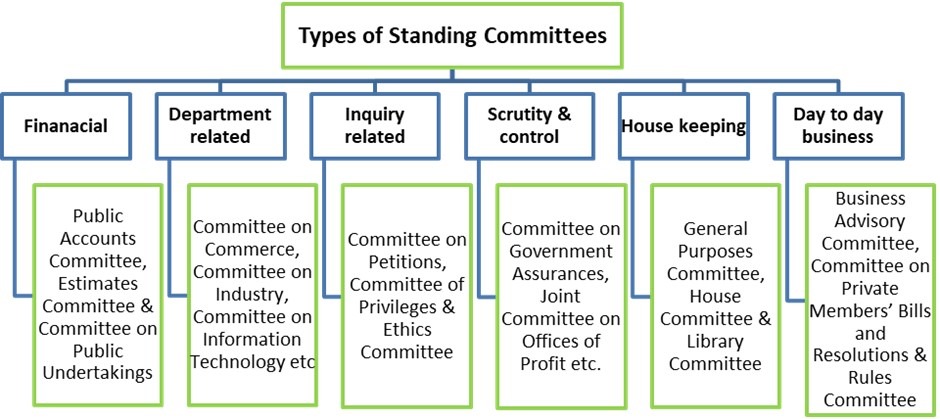

Committees to Inquire:

- These include the Committee on Petitions, Committee on Privileges, and the Ethics Committee.

Committees to Scrutinise and Control:

- These include the Committee on Government Assurances, Committee on Subordinate Legislation, and Committee on Papers Laid on the Table.

Committees Relating to the Day-to-Day Business of the House:

- These include the Business Advisory Committee, Committee on Private Members’ Bills and Resolutions, and the Rules Committee.

House-Keeping Committees or Service Committees:

- These deal with members’ facilities and services, such as the General Purposes Committee, House Committee, and Library Committee.

The specific examples of Departmental Standing Committees, including the Committee on Coal and Steel (dealing with Coal, Mines, and Steel) and the Committee on Social Justice and Empowerment (dealing with Social Justice and Empowerment, Tribal Affairs, and Minority Affairs).